S-3: Registration statement for specified transactions by certain issuers

Published on December 18, 2017

AS FILED WITH THE SECURITIES AND EXCHANGE COMMISSION ON DECEMBER 18, 2017

REGISTRATION NO. 333-_________

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM S-3

REGISTRATION STATEMENT UNDER THE SECURITIES ACT OF 1933

MARATHON PATENT GROUP, INC.

(Exact name of registrant as specified in its charter)

Nevada

(State or other jurisdiction of incorporation or organization)

01-0949984

I.R.S. Employer Identification Number

11601 Wilshire Blvd., Ste. 500

Los Angeles, CA 90025

(703) 232-1701

(Address, including zip code, and telephone number, including area code of registrant’s principal executive offices)

Copies to:

Harvey J. Kesner, Esq.

Arthur S. Marcus, Esq.

Sichenzia Ross Ference Kesner LLP

1185 Avenue of the Americas, Suite 3700

New York, New York 10036

Phone: (212) 930-9700

Fax: (212) 930-9725

Approximate date of commencement of proposed sale to the public: From time to time after the effective date of this registration statement.

If the only securities being registered on this Form are being offered pursuant to dividend or interest reinvestment plans, please check the following box: [ ]

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, as amended (the “Securities Act”) other than securities offered only in connection with dividend or interest reinvestment plants, check the following box: [X]

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, please check the following and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. [ ]

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. [ ]

If this Form is a registration statement pursuant to General Instruction I.D. or a post-effective amendment thereto that shall become effective upon filing with the Commission pursuant to Rule 462(e) under the Securities Act, check the following box. [ ]

If this Form is a post-effective amendment to a registration statement filed pursuant to General Instruction I.D. filed to register additional securities or additional classes of securities pursuant to Rule 413(b) under the Securities Act, check the following box. [ ]

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act. (Check one):

| Large accelerated filer [ ] | Accelerated filer [ ] | Non-accelerated filer [ ] | Smaller reporting company [X] |

|

(Do

not check if a smaller reporting company) |

|||

| Emerging growth company [ ] |

| Title

of each class of securities to be registered |

Amount to be registered(1) |

Proposed |

Proposed maximum aggregate offering price(2) |

Amount

of registration fee(2) |

||||||||||||

| Common Stock, par value $0.0001 per share | ||||||||||||||||

| (a) Shares pursuant to the issuance of | ||||||||||||||||

| Convertible Notes. | 2,808,875 | $ | 5.62 | $ | 15,785,877.50 | $ | 1,965.34 | |||||||||

| (b) Shares issued to our counsel in | ||||||||||||||||

| settlement of outstanding legal fees | 20,000 | $ | 5.62 | $ | 112,400.00 | $ | 13.99 | |||||||||

| Shares already issued by registrant. | 2,828,875 | $ | 5.62 | $ | 15,898,277.50 | $ | 1, 979.33 | |||||||||

| (1) |

Pursuant to Rule 415 under the Securities Act this registration statement shall be deemed to cover an indeterminate number of additional securities to be offered as a result of stock splits, stock dividends or similar transactions. The shares may be offered for resale by the selling stockholders pursuant to the shelf prospectus contained herein. |

| (2) |

Estimated solely for the purpose of computing the amount of the registration fee pursuant to Rule 457(c) under the Securities Act, based on an average of the high and low reported sales prices of the registrant’s shares of common stock, as reported on the NASDAQ Capital Market on December 14, 2017 of $5.95 and $5.29, respectively. |

The registrant hereby amends this Registration Statement on such date or dates as may be necessary to delay its effective date until the registrant shall file a further amendment which specifically states that this Registration Statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act or until this Registration Statement shall become effective on such date as the Securities and Exchange Commission (the “Commission”), acting pursuant to said Section 8(a), may determine.

The information in this prospectus is not complete and may be changed. The selling stockholders may not sell these securities under this prospectus until the registration statement of which it is a part and filed with the Securities and Exchange Commission is effective. This prospectus is not an offer to sell these securities and it is not soliciting an offer to buy these securities in any state where the offer or sale is not permitted.

PRELIMINARY PROSPECTUS, SUBJECT TO COMPLETION, DATED DECEMBER 18, 2017

MARATHON PATENT GROUP INC.

2,828,875 Shares of Common Stock

This prospectus relates to the resale of up to 2,828,875 shares of common stock, par value $0.0001 per share (the “Common Stock”) of Marathon Patent Group, Inc. (the “Company”) by the selling stockholders, representing (i) 2,808,875 shares issuable upon conversion of the Company’s 5% convertible promissory notes (the “Convertible Notes”); and (ii) 20,000 shares of Common Stock already issued by the Company, being registered herein. The Convertible Notes were issued pursuant to a private placement by the Company in August 2017.

The selling stockholders may sell Common Stock from time to time in the principal market on which the stock is traded at the prevailing market price or in negotiated transactions.

We will not receive any of the proceeds from the sale of Common Stock by the selling stockholders. We will pay the expenses of registering these shares.

Investing in our Common Stock involves a high degree of risk. You should consider carefully the risk factors beginning on page 7 of this prospectus before purchasing any of the shares offered by this prospectus.

Our Common Stock is listed on the NASDAQ Capital Market under the symbol “MARA”.

The last reported sale price of our Common Stock on the NASDAQ Capital Market on December 14, 2017 was $5.43 per share.

We may amend or supplement this prospectus from time to time by filing amendments or supplements as required. You should read the entire prospectus and any amendments or supplements carefully before you make your investment decision.

Neither the Securities and Exchange Commission (the “Commission”) nor any state securities commission has approved or disapproved of these securities or determined if this prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

The date of this prospectus is December 18, 2017.

TABLE OF CONTENTS

You may only rely on the information contained in this prospectus or that we have referred you to. We have not authorized anyone to provide you with different information. This prospectus does not constitute an offer to sell or a solicitation of an offer to buy any securities other than the Common Stock offered by this prospectus. This prospectus does not constitute an offer to sell or a solicitation of an offer to buy any Common Stock in any circumstances in which such offer or solicitation is unlawful. Neither the delivery of this prospectus nor any sale made in connection with this prospectus shall, under any circumstances, create any implication that there has been no change in our affairs since the date of this prospectus or that the information contained by reference to this prospectus is correct as of any time after its date.

This summary highlights information contained elsewhere in this prospectus. You should read the entire prospectus carefully, including the section entitled “Risk Factors” before deciding to invest in our Common Stock. The terms “Marathon,” the “Company,” “we,” “our” or “us” in this prospectus refer to Marathon Patent Group, Inc. and its wholly-owned subsidiaries, unless the context suggests otherwise.

About Marathon Patent Group, Inc.

In November 2012, we changed our name to Marathon Patent Group, Inc. and commenced business seeking to enforce and license patents, engaging in the business known as patent monetization. On November 1, 2017, we entered into an agreement to acquire 100% of the capital stock of Global Bit Ventures, Inc. (“GBV”), which owns and operates specialized computer equipment in Canada to secure the blockchain and generate digital assets often referred to as “cryptocurrency”, such as bitcoin and ether. See “Risk Factors – Risks Related to the Merger”; “Risk Factors - Risks Related to the Business of GBV Upon Completion of the Merger”.

We were incorporated in the State of Nevada on February 23, 2010 under the name “Verve Ventures, Inc.” On December 7, 2011, we changed our name to “American Strategic Minerals Corporation”.

| 3 |

Description of Business

The Company maintains a portfolio of patents. We acquired patents and patent rights from owners or other ventures and sought to monetize the value of the patents through litigation and licensing strategies, alone or with others. As of December 15, 2017, we owned 86 patents, which include U.S. patents and foreign patents. The Company and certain of its subsidiaries entered into a First Amendment to Amended and Restated Revenue Sharing and Securities Purchase Agreement and Restructuring Agreement dated August 3, 2017 (the “First Amendment and Restructuring Agreement”), with DBD Credit Funding LLC (“DBD”) to restructure and replace the obligations of Marathon under an Amended and Restated Revenue Sharing and Securities Purchase Agreement, dated January 10, 2017, amending the original agreement entered into by the Company and DBD on January 29, 2015. As contemplated in the First Amendment and Restructuring Agreement, in connection with the elimination of our long-term debt to DBD, on October 20, 2017, we entered into agreements with DBD and assigned several of its patents to a special purpose entity managed by DBD.

On October 20, 2017, we closed the First Amendment and Restructuring Agreement with DBD to restructure and replace the obligations of the Company under that certain Amended and Restated Revenue Sharing and Securities Purchase Agreement, dated January 10, 2017, which was originally entered into on January 29, 2015. Pursuant to the First Amendment and Restructuring Agreement, certain patents were assigned to the newly created special purpose entity (the “SPE”) elected by DBD, which SPE is under the management and control of an affiliate of DBD. As a result, DBD now has full, direct control over the patents under the SPE structure. Our interest of 30% of the SPE may not have any value after the recoupment of DBD’s investment and its costs and expenses. We retain no control over, ownership of, or recourse to, the SPE patents. As a result, we are wholly-dependent on the efforts and experience of DBD, as well as the costs associated with the efforts of DBD, for any recoveries under these patents as to which we do not anticipate receiving any.

In connection with the Company’s agreement to acquire GBV, the Company has secured financing in connection with winding down the patenting business and working capital for reduced operations while it prepares for the acquisition of GBV. The Company is transitioning from its historic business into businesses involved in supporting the blockchain and digital asset (cryptocurrency) ecosystem. While reducing its reliance on patent enforcement and licensing for the generation of revenue, the Company has undertaken steps to dedicate its resources and efforts towards blockchain and digital asset (cryptocurrency) acquisition. Cryptocurrencies are one form of digital assets. As a result, we sometimes use the phrases “cryptocurrency” and “digital assets” interchangeably. These activities include the acquisition of businesses and assets engaged in or necessary for supporting the business of mining, as described below, including the direct acquisition of businesses, equipment and technology that service the blockchain ecosystem as well as the outright acquisition of digital assets, such as cryptocurrency, that may be held for appreciation or exchanged for other assets or sold. The Company intends to complete the acquisition of GBV and enter into a new and unproven business model with significant risks, both known and unknown, as more fully described in the section titled Risk Factors, below. In connection with that newly-adopted business strategy, the Company anticipates it will be necessary to add personnel to the management team, as well as other personnel, to enhance assessment of controls over risks, to review and seek approval of regulatory bodies (including the NASDAQ Capital Market for continued listing of its Common Stock) and will face other uncertainties associated with the evolving business and regulatory risks of blockchain and digital assets (cryptocurrency). There is no assurance that the Company will be able to successfully navigate these risks or that regulatory and other requirements will not have a material adverse effect on the goals and objectives of the Company or prevent the Company from realizing its objectives.

Founded in 2017, GBV is a digital asset mining company. GBV intends to power and secure the blockchain by verifying blockchain transactions using custom hardware and software. GBV intends to use their hardware to mine bitcoin (BTC) and ether (ETH), two different forms of digital assets. GBV will be compensated in digital assets by the respective blockchain network that it secures for its efforts, which is how GBV generates revenue.

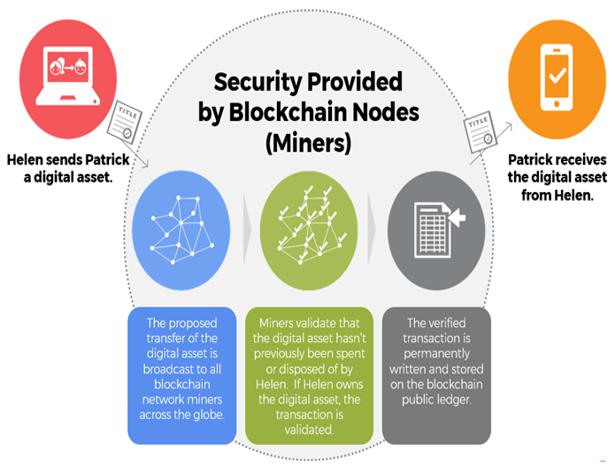

Blockchains are decentralized digital ledgers that record and enable secure peer-to-peer transactions without third party intermediaries. Blockchains enable the existence of digital assets by allowing participants to confirm transactions without the need for a central certifying authority. When a participant requests a transaction, a peer-to-peer network consisting of computers, known as nodes, validate the transaction and the user’s status using known algorithms. After the transaction is verified, it is combined with other transactions to create a new block of data for the ledger. The new block is added to the existing blockchain in a way that is permanent and unalterable, and the transaction is complete. The following illustration outlines the process of a transaction between two digital asset holders.

| 4 |

Digital assets (also known as cryptocurrency) is a medium of exchange that uses encryption techniques to control the creation of monetary units and to verify the transfer of funds. Many consumers use digital assets because it offers cheaper and faster peer-to-peer payment options without the need to provide personal details. Every single transaction made and the ownership of every single digital asset in circulation is recorded in the blockchain. Miners use powerful computers that tally the transactions to run the blockchain. These miners update each time a transaction is made and ensure the authenticity of information. The miners receive a transaction fee for their service in the form of a portion of the new digital “coins” that are issued. Bitcoin is the most well-known digital asset, while ether is another type of digital asset.

Blockchain based transactions can involve digital assets, contracts, records, or other information.

Mining digital assets typically requires a substantial amount of specialized computer hardware and server equipment including a cost-effective data center to house the hardware. GBV is utilizing a datacenter based in Quebec Canada to house and run its equipment in order to meet the requirements to mine bitcoin and ether.

As a condition to the Merger, all of the Company’s existing outstanding debt, consisting of the Convertible Notes, in the aggregate amount of $4,053,948 (the “Company Debt”) shall be cancelled in exchange for the Company’s Series E-1 Convertible Preferred Stock in a transaction pursuant to Section 3(a)(9) of the Securities Act, and as of the closing of the Merger, the Company shall not have any outstanding Company Debt. The terms of the Series E-1 Convertible Preferred Stock are set forth in the Proposed Certificate of Designation of Preferences, Rights and Limitations of the 0% E-1 Convertible Preferred Stock, substantially in the form attached hereto as Exhibit 3.8 of this Prospectus.

Company Information

Our principal office is located at 11601 Wilshire Blvd., Ste. 500, Los Angeles, California 90025. Our telephone number is (703) 232-1701. Our Internet address is www.marathonpg.com. Information on our website is not incorporated into this prospectus supplement or the accompanying prospectus and should not be relied upon in connection with making any investment decision with respect to the securities offered by this prospectus supplement and the accompanying prospectus.

| 5 |

About This Offering

This Prospectus relates to the resale of up to 2,828,875 shares of our Common Stock by the selling shareholders, representing (i) 753,519 shares issuable upon conversion of Convertible Notes; and (ii) 20,000 shares of Common Stock already issued by the Company, being registered herein. The Convertible Notes were issued pursuant to a private placement by the Company in August 2017. The Company registered 1,848,500 shares of Common Stock including the resale of 1,649,000 shares issuable upon conversion of the Convertible Notes pursuant to a Registration Statement on Form S-3 (File No. 333-220438) which was declared effective on October 13, 2017, by the Commission. As of December 15, 2017, 11,123,235 shares of Common Stock were issued and outstanding, one share of our Series B Convertible Preferred Stock (the “Series B Preferred Stock”) was issued and outstanding and 5,480.65 shares of our Series E Convertible Preferred Stock (the “Series E Preferred Stock”) were issued and outstanding.

The Company entered into separate unit purchase agreements (the “Unit Purchase Agreement”) with accredited investors (the “Purchasers”) providing for sale of up to $5,500,000 of Convertible Notes and five-year warrants, including the Exchange Warrants, to purchase such number of shares of Common Stock as shall be issuable upon exercise of the Convertible Notes, at an exercise price equal to $1.20 per share (the “Warrants”). The conversion price of the Convertible Notes is equal to the lesser of $0.80 per share or the closing bid price (as reported on the NASDAQ Capital Market) of the Common Stock on the day prior to conversion of the Convertible Note, but not less than $0.40 per share. The Warrants (prior to exchange for Series E Preferred Stock) are exercisable at a price of $1.20 per share of Common Stock. The Convertible Notes and Warrants sold pursuant to the Unit Purchase Agreements provide for adjustment of the conversion and exercise prices upon the issuance of equity or equity-linked securities of the Company at prices lower than the respective conversion or exercise prices of the Convertible Notes and Warrants, respectively. The Series E Preferred Stock issued upon exchange of the Exchange Warrants does not contain anti-dilution protection upon the issuance of lower priced equity or equity-linked securities by the Company.

The Convertible Notes bear interest at five (5%) percent per annum with interest payable in cash upon maturity or in connection with any voluntary or mandatory conversion. The Convertible Notes are convertible, in whole or in part, into shares of Common Stock at the option of the Noteholders, at any time and from time to time after the date of issuance and until the Convertible Note is no longer outstanding, subject to a 4.99% beneficial ownership limitation. Upon not less than 61 days’ prior notice to the Company, the Noteholder may increase the beneficial ownership limitation, provided that the beneficial ownership limitation in no event exceeds 9.99% of the Common Stock outstanding immediately after giving effect to the issuance of Common Stock upon conversion of the Convertible Notes.

| 6 |

The combined organization will be faced with a market environment that cannot be predicted and that involves significant risks, many of which will be beyond its control. In addition to the other information contained in this proxy statement/prospectus/information statement, you should carefully consider the material risks described below before deciding how to vote your shares of stock. In addition, you should read and consider the risks associated with Marathon’s business because these risks may also affect the combined organization — these risks can be found under the heading “Risk Factors — Risks Related to Marathon” in this proxy statement/prospectus/information statement and in Marathon’s Current Report on Form 8-K filed with the SEC November 2, 2017 and other filings and reports by Marathon with the SEC and incorporated by reference into this proxy statement/prospectus/information statement. You should also read and consider the other information in this proxy statement/prospectus/information statement and the other documents incorporated by reference into this proxy statement/prospectus/information statement. Please see the section entitled “Where You Can Find More Information” in this proxy statement/prospectus/information statement.

Risks Related to the Merger

The exchange ratio is not adjustable based on the market price of Marathon Common Stock, so the Merger consideration at the closing may have a greater or lesser value than at the time the Merger Agreement was signed.

The Merger Agreement has set the exchange ratio for the GBV capital stock, and the exchange ratio is based on the outstanding capital stock of GBV and the outstanding Common Stock of Marathon, in each case, at the time of execution of the Merger Agreement as described under the heading “The Merger—Merger Consideration.” Any changes in the outstanding capital stock or market price of Marathon Common Stock before the completion of the Merger will not affect the number of shares of Marathon Series C Preferred Stock or Marathon Common Stock issuable to GBVs shareholders pursuant to the Merger Agreement. Therefore, if before the completion of the Merger the market price of Marathon Common Stock declines from the market price on the date of the Merger Agreement, then GBV’s shareholders could receive Merger consideration with substantially lower value than the value of the Merger consideration on the date of the Merger Agreement. Similarly, if before the completion of the Merger the market price of Marathon Common Stock increases from the market price of Marathon’s Common Stock on the date of the Merger Agreement, then GBV’s shareholders could receive Merger consideration with substantially greater value than the value of such Merger consideration on the date of the Merger Agreement. The Merger Agreement does not include a price-based termination right. Because the exchange ratio does not adjust as a result of changes in the outstanding capital stock or market price of Marathon’s Common Stock.

Failure to complete the Merger could significantly harm the market price of Marathon Common Stock and negatively affect the future business and operations of each company.

If the Merger is not completed and the Merger Agreement is terminated expenses are not reimbursable in connection with a termination of the Merger Agreement, each of Marathon and GBV will have incurred significant fees and expenses, such as legal and accounting fees which Marathon and GBV estimate will total approximately $750,000 and $150,000, respectively, which must be paid whether or not the Merger is completed. Further, if the Merger is not completed, it could significantly harm the market price of Marathon’s Common Stock.

In addition, if the Merger Agreement is terminated and the board of directors of Marathon or GBV determines to seek another business combination, there can be no assurance that either Marathon or GBV will be able to find a partner and close an alternative transaction on terms that are as favorable or more favorable than the terms set forth in the Merger Agreement.

| 7 |

The Merger may be completed even though certain events occur prior to the closing that materially and adversely affect Marathon or GBV.

The Merger Agreement provides that either Marathon or GBV can refuse to complete the Merger. However, certain types of changes do not permit either party to refuse to complete the Merger, even if such change could be said to have a material adverse effect on Marathon or GBV, including:

| ● | any effect resulting from the announcement or pendency of the Merger or any related transactions; | |

| ● | the taking of any action, or the failure to take any action, by either Marathon or GBV required to comply with the terms of the Merger Agreement; | |

| ● | any natural disaster or any act or threat of terrorism or war anywhere in the world, any armed hostilities or terrorist activities anywhere in the world, any threat or escalation or armed hostilities or terrorist activities anywhere in the world, or any governmental or other response or reaction to any of the foregoing; | |

| ● | general economic or political conditions or conditions generally affecting the industries in which Marathon or GBV, as applicable, operates; | |

| ● | any illegality or rejection by a governmental body, of the blockchain or digital asset industry, or changes in the prices of digital assets; | |

| ● | any change in accounting requirements, tax treatment or principles or any change in applicable laws, rules, or regulations or the interpretation thereof; | |

| ● | with respect to Marathon, any change in the stock price or trading volume of Marathon’s Common Stock excluding any underlying effect that may have caused such change; | |

| ● | with respect to GBV, the termination, sublease, or assignment or disruption in the facility arrangements involving Hypertec or other location housing the business or operations of GBV; | |

| ● | with respect to Marathon, continued losses from operations or decreases in cash balances of Marathon not materially inconsistent with kind and degree of losses from operations and decreases in cash balances which have occurred since September 30, 2017, unfavorable outcome or commencement of any litigation or claims against Marathon; | |

| ● | with respect to Marathon, the winding down of Marathon’s operations not materially inconsistent with the kind and degree of winding down activities which have occurred since September 30, 2017; and | |

| ● | with respect to GBV and Marathon, any change in the cash position of GBV or Marathon resulting from operations in the ordinary course of business. |

If adverse changes occur and Marathon and GBV still complete the Merger, the market price of the combined organization’s Common Stock may suffer. This in turn may reduce the value of the Merger to the shareholders of Marathon, GBV or both.

Some Marathon and GBV officers and directors have interests in the Merger that are different from yours and that may influence them to support or approve the Merger without regard to your interests.

Certain officers and directors of Marathon and GBV participate in arrangements that provide them with interests in the Merger that are different from yours, including, among others, the continued service as an officer or director of the combined organization, severance benefits, the acceleration of stock option vesting, continued indemnification and the potential ability to sell an increased number of shares of common stock of the combined organization in accordance with Rule 144 under the Securities Act of 1933, as amended (“Securities Act”).

For example, Marathon has entered into certain employment and severance benefits arrangements with certain of its executive officers, including Doug Croxall and Francis Knuettel II, that may result in the receipt by such executive officers of cash severance payments and restricted stock and other benefits, including benefits which become effective upon the closing of the Merger Agreement

| 8 |

In addition, and for example, certain of GBV’s directors and officers, including Charles Allen and Jesse Sutton, have ownership of GBV capital stock which, at the closing of the Merger, shall be converted into and become shares of Series C Preferred Stock or Common Stock of Marathon, certain of GBV’s directors and officers are expected to become directors and officers of Marathon upon the closing of the Merger, and all of GBV’s directors and officers are entitled to certain indemnification and liability insurance coverage as a result of the closing of the Merger. These interests, among others, may influence the officers and directors of Marathon and GBV to support or approve the Merger.

For more information concerning the interests of Marathon’s and GBV’s officers and directors, see the sections entitled “The Merger—Interests of Marathon Directors and Officers in the Merger” and “The Merger—Interests of GBV Directors and Officers in the Merger” in this proxy statement/prospectus/information statement.

The market price of Marathon’s Common Stock following the Merger may decline as a result of the Merger.

The market price of Marathon’s Common Stock may decline as a result of the Merger for a number of reasons including if:

| ● | investors react negatively to the prospects of the combined organization, business and financial condition following the Merger; | |

| ● | the effect of the Merger on the combined organization’s business and prospects is not consistent with the expectations of financial or industry analysts; or | |

| ● | the combined organization does not achieve the perceived benefits of the Merger as rapidly or to the extent anticipated by financial or industry analysts. |

Marathon and GBV shareholders may not realize a benefit from the Merger commensurate with the ownership dilution they will experience in connection with the Merger.

If the combined organization is unable to realize the strategic and financial benefits currently anticipated from the Merger, Marathon and GBV’s shareholders will have experienced substantial dilution of their ownership interests in their respective companies without receiving the expected commensurate benefit, or only receiving part of the commensurate benefit to the extent the combined organization is able to realize only part of the expected strategic and financial benefits currently anticipated from the Merger.

During the pendency of the Merger, Marathon and GBV may not be able to enter into a business combination with another party at a favorable price because of restrictions in the Merger Agreement, which could adversely affect their respective businesses.

Covenants in the Merger Agreement impede the ability of Marathon and GBV to make acquisitions, subject to certain exceptions relating to fiduciary duties, or to complete other transactions that are not in the ordinary course of business pending completion of the Merger. As a result, if the Merger is not completed, the parties may be at a disadvantage to their competitors during such period. In addition, while the Merger Agreement is in effect, each party is generally prohibited from soliciting, initiating, encouraging or entering into certain extraordinary transactions, such as a Merger, sale of assets, or other business combination outside the ordinary course of business with any third party, subject to certain exceptions relating to fiduciary duties. Any such transactions could be favorable to such party’s shareholders.

Certain provisions of the Merger Agreement may discourage third parties from submitting alternative takeover proposals, including proposals that may be superior to the arrangements contemplated by the Merger Agreement.

The terms of the Merger Agreement prohibit each of Marathon and GBV from soliciting alternative takeover proposals or cooperating with persons making unsolicited takeover proposals, except in limited circumstances when such party’s board of directors determines in good faith that an unsolicited alternative takeover proposal is or is reasonably likely to lead to a superior takeover proposal and that failure to cooperate with the proponent of the proposal would be reasonably likely to be inconsistent with the board’s fiduciary duties. Moreover, even if a party receives what the party’s board of directors determines is a superior proposal, the Merger Agreement does not permit either party to terminate the Merger Agreement to enter into a superior proposal.

| 9 |

Because the lack of a public market for GBV’s capital stock and notes makes it difficult to evaluate the value of GBV’s capital stock, the shareholders of GBV may receive shares of Marathon’s Series C Preferred Stock or Common Stock in the Merger that have a value that is less than, or greater than, the fair market value of GBV’s capital stock or notes.

The outstanding capital stock of GBV (and the GBV Notes) are privately held and is not traded in any public market. The lack of a public market makes it extremely difficult to determine the fair market value of GBV. Because the percentage of Marathon’s Series C Preferred Stock or Common Stock to be issued to GBV’s shareholders and the GBV Note holders was determined based on negotiations between the parties, it is possible that the value of Marathon’s Series C Preferred Stock and Common Stock to be received by GBV’s shareholders and note holders will be less than the fair market value of GBV, or Marathon may pay more than the aggregate fair market value for GBV.

If the conditions to the Merger are not met, the Merger will not occur.

Even if the Merger is approved by the shareholders of Marathon and GBV, specified conditions must be satisfied or waived to complete the Merger. These conditions are set forth in the Merger Agreement and described in the section entitled “The Merger Agreement—Conditions to the Completion of the Merger” in this proxy statement/prospectus/information statement. Marathon and GBV cannot assure you that all of the conditions will be satisfied or waived. If the conditions are not satisfied or waived, the Merger will not occur or will be delayed, and Marathon and GBV each may lose some, or all, of the intended benefits of the Merger.

Risks Related to Marathon

We may not be able to successfully monetize our patents and thus we may fail to realize all of the anticipated benefits of such acquisitions.

There is no assurance that Marathon will be able to continue to successfully acquire, develop or monetize its patent portfolio. The acquisition of patents could fail to produce anticipated benefits or there could be other adverse effects that we do not currently foresee. Failure to successfully monetize our patents would have a material adverse effect on our business, financial condition and results of operations. We have ceased acquiring new patents and have significantly reduced our workforce and activities seeking to monetize patents.

In addition, our patent portfolio is subject to a number of risks, including, but not limited to the following:

| ● | There is a significant time lag between acquiring a patent portfolio and recognizing revenue from such patent asset. During such time lag, substantial amounts of costs are likely to be incurred that could have a negative effect on our results of operations, cash flows and financial position; | |

| ● | The monetization of a patent portfolio is a time consuming and expensive process that may disrupt our operations. If our monetization efforts are not successful, our results of operations could be harmed. In addition, we may not achieve anticipated synergies or other benefits from such acquisition; and | |

| ● | We may encounter unforeseen difficulties with our business or operations in the future that may deplete our capital resources more rapidly than anticipated. As a result, we may be required to obtain additional working capital in the future through public or private debt or equity financings, borrowings or otherwise. If we are required to raise additional working capital in the future, such financing may be unavailable to us on favorable terms, if at all, or may be dilutive to our existing shareholders. If we fail to obtain additional working capital, as and when needed, such failure could have a material adverse impact on our business, results of operations and financial condition. |

| 10 |

Therefore, there is no assurance that the monetization of our patent portfolios will generate enough revenue to recoup our investment.

On October 20, 2017, we closed the First Amendment and Restructuring Agreement with DBD to restructure and replace the obligations of Marathon under that certain Amended and Restated Revenue Sharing and Securities Purchase Agreement, dated January 10, 2017, which was originally entered into on January 29, 2015. Pursuant to the First Amendment and Restructuring Agreement, certain patents were assigned to the newly created special purpose entity, an SPE elected by DBD, which SPE is under the management and control of an affiliate of DBD. As a result, DBD now has full, direct control over the patents under the SPE structure. Our interest of 30% of the SPE may not have any value after the recoupment of DBD’s investment and its costs and expenses. We retain no control over, ownership of, or recourse to, the SPE patents. As a result, we are wholly-dependent on the efforts and experience of DBD, as well as the costs associated with the efforts of DBD, for any recoveries under these patents as to which we do not anticipate receiving any. After creation of the SPE and as of December 15, 2017, we owned 86 patents.

We presently rely upon the patent assets we acquire from other patent owners. If we are unable to monetize such assets and generate revenue and profit through those assets or by other means, there is a significant risk that our business would fail.

When we commenced our current line of business in 2012, we acquired a portfolio of patent assets from Sampo IP, LLC (“Sampo”), a company affiliated with our Chief Executive Officer, Douglas Croxall, from which we have generated revenue from enforcement activities. On April 16, 2013, we acquired a patent from Mosaid Technologies Incorporated, a Canadian corporation. On April 22, 2013, we acquired a patent portfolio through a Merger between our wholly-owned subsidiary, CyberFone Acquisition Corp., a Texas corporation and CyberFone Systems LLC, a Texas limited liability company (“CyberFone Systems”). In June 2013, in connection with the closing of a licensing agreement with Siemens Technology, Inc. (“Siemens”), we acquired a patent portfolio. In September 2013, we acquired a portfolio from TeleCommunication Systems and an additional portfolio from Intergraph Corporation. In October 2013, we acquired a patent portfolio from TT IP, LLC. In December 2013 we engaged in three transactions: (i) in connection with a licensing agreement with Zhone Technologies Inc., we acquired a portfolio of patents from that company; (ii) we acquired a patent portfolio from Delphi Technologies, Inc.; and (iii) in connection with a settlement and license agreement, we agreed to settle and release a defendant for past and future use of our patents, whereby the defendant agreed to assign and transfer two U.S. patents and rights to us. In May 2014, we acquired ownership rights of Dynamic Advances, LLC, a Texas limited liability company, IP Liquidity Ventures, LLC, a Delaware limited liability company and Sarif Biomedical, LLC, a Delaware limited liability company, all of which hold patent portfolios or contract rights to the revenue generated from patent portfolios. In June 2014, we acquired Selene Communication Technologies, LLC, which holds multiple patents in the search and network intrusion field. In August 2014, we acquired patents from Clouding IP LLC, with such patents related to network and data management technology. In September 2014, we acquired TLI Communications, which owns a single patent in the telecommunication field. In October 2014, we acquired three patent portfolios from MedTech Development, LLC, which owns medical technology patents. In June 2016, one of our subsidiaries, Munitech S.a.r.l. (“Munitech”), acquired two patent portfolios from Siemens covering W-CDMA and GSM cellular technology. In July 2016, one of our subsidiaries, Magnus GmbH (“Magnus”), acquired a patent portfolio from Siemens covering internet-of-things technology. In August 2016, we entered into two transactions. In the first, we acquired a patent portfolio from CPT IP Holdings, LLC covering battery technology and in the second, we entered into a Patent Funding and Exclusive License Agreement with a Fortune 50 company to monetize more than 10,000 patents in a single industry vertical. In September 2016, one of our subsidiaries, Motheye Technologies, LLC (“Motheye”), acquired a patent from Cirrex Systems, LLC, covering LED technology; however, in June 2017, following a decision by Marathon not to enforce such patent, Motheye entered into an agreement whereby such patent held by the subsidiary was assigned back to Cirrex Systems, LLC. In September 2017, Marathon sold Munitech, which included both its assets and its liabilities, in a private transaction to a third party.

Following the closing of the Merger, and giving effect to the SPE, we no longer may generate revenues from our acquired patent portfolios, several of which have been disposed of and others are inactive. If our efforts to generate revenue from these assets fail, we will have incurred significant losses and may be unable to acquire additional assets. If this occurs, our patent monetization business would likely fail.

| 11 |

We have economic interests in patent portfolios that we do not control and the decision regarding the timing and amount of licenses are held by third parties, which could lead to outcomes materially different than what we intended.

We own contract rights to patent portfolios (including the SPE) over which we do not exercise control and cannot determine when and if, and if so, for how much, the patent owner licenses the patents. This could lead to situations where we have dedicated resources, time and money to portfolios that provide little or no return on our investment. In these situations, we would record a loss on investment and incur losses that contribute to our overall performance and could have a material adverse impact on its financial condition.

Failure to effectively manage our growth could place strains on our managerial, operational and financial resources and could adversely affect our business and operating results.

Our growth has placed, and is expected to continue to place, a strain on our limited managerial, operational and financial resources and systems. Further, as our subsidiary companies’ businesses grow, we will be required to continue to manage multiple relationships. Any further growth by us or our subsidiary companies, or an increase in the number of our strategic relationships, may place additional strain on our managerial, operational and financial resources and systems. Although we may not grow as we expect, if we fail to manage our growth effectively or to develop and expand our managerial, operational and financial resources and systems, our business and financial results would be materially harmed.

We initiate legal proceedings against potentially infringing companies in the normal course of our business and we believe that extended litigation proceedings would be time-consuming and costly, which may adversely affect our financial condition and our ability to operate our business.

To monetize our patent assets, we historically have initiated legal proceedings against potential infringing companies, pursuant to which we may allege that such companies infringe on one or more of our patents. Our viability could be highly dependent on the cost and outcome of the litigation, and there is a risk that we may be unable to achieve the results we desire from such litigation, which failure would substantially harm our business. In addition, the defendants in the litigations are likely to be much larger than us and have substantially more resources than we do, which could make our litigation efforts more difficult and impact the duration of the litigation which would require us to devote our limited financial, managerial and other resources to support litigation that may be disproportionate to the anticipated recovery.

These legal proceedings may continue for several years and may require significant expenditures for legal fees, patent related costs, such as inter-partes review, and other expenses. Disputes regarding the assertion of patents and other intellectual property rights are highly complex and technical. Once initiated, we may be forced to litigate against others to enforce or defend our patent rights or to determine the validity and scope of other party’s patent rights. The defendants or other third parties involved in the lawsuits in which we are involved may allege defenses and/or file counterclaims or commence re-examination proceedings by patenting issuance authorities in an effort to avoid or limit liability and damages for patent infringement, or declare our patents to be invalid or non-infringed. If such defenses or counterclaims are successful, they may preclude our ability to derive revenue from the patents we own. A negative outcome of any such litigation, or an outcome which affects one or more claims contained within any such litigation or invalidating any patents, could materially and adversely impact our business. Additionally, we anticipate that our legal fees and other expenses will be material and will negatively impact our financial condition and results of operations and may result in our inability to continue our business. We have incurred significant legal expenses in our patent litigation in the past that are liabilities of the Company and may be unable to settle or reduce these expenses, regardless of the outcome of our patent litigation or the inability to license or recover damages from our patents. These liabilities may continue following the Merger and lead to litigation or claims with respect to the payment or collection of legal expenses.

| 12 |

Variability in intellectual property laws may adversely affect our intellectual property position.

Intellectual property laws, and patent laws and regulations in particular, have been subject to significant variability either through administrative or legislative changes to such laws or regulations or changes or differences in judicial interpretation, and it is expected that such variability will continue to occur. Additionally, intellectual property laws and regulations differ among states, and countries. Variations in the patent laws and regulations or in interpretations of patent laws and regulations in the United States and other countries may diminish the value of our intellectual property and may change the impact of third-party intellectual property on us. Accordingly, we cannot predict the scope of patents that may be granted to us, the extent to which we will be able to enforce our patents against third parties, or the extent to which third parties may be able to enforce their patents against us.

We may seek to internally develop additional new inventions and intellectual property, which would take time and be costly. Moreover, the failure to obtain or maintain intellectual property rights for such inventions would lead to the loss of our investments in such activities.

We may in the future seek to engage in commercial business ventures or seek internal development of new inventions or intellectual property. These activities would require significant amounts of financial, managerial and other resources and would take time to achieve. Such activities could also distract our management team from its present business initiatives, which could have a material and adverse effect on our business. There is also the risk that such initiatives may not yield any viable new business or revenue, inventions or technology, which would lead to a loss of our investment in such activities.

In addition, even if we are able to internally develop new inventions, in order for those inventions to be viable and to compete effectively, we would need to develop and maintain, and we would be heavily reliant upon, a proprietary position with respect to such inventions and intellectual property. However, there are significant risks associated with any such intellectual property we may develop principally including the following:

| ● | patent applications we may file may not result in issued patents or may take longer than we expect to result in issued patents; | |

| ● | we may be subject to interference proceedings; | |

| ● | we may be subject to opposition proceedings in the U.S. or foreign countries; | |

| ● | any patents that are issued to us may not provide meaningful protection; | |

| ● | we may not be able to develop additional proprietary technologies that are patentable; | |

| ● | other companies may challenge patents issued to us; | |

| ● | other companies may have independently developed and/or patented (or may in the future independently develop and patent) similar or alternative technologies, or duplicate our technologies; | |

| ● | other companies may design around technologies we have developed; and | |

| ● | enforcement of our patents would be complex, uncertain and very expensive. |

| 13 |

We cannot be certain that patents will be issued as a result of any future patent applications, or that any of our patents, once issued, will provide us with adequate protection from competing products. For example, issued patents may be circumvented or challenged, declared invalid or unenforceable or narrowed in scope. In addition, since publication of discoveries in scientific or patent literature often lags behind actual discoveries, we cannot be certain that we will be the first to make our additional new inventions or to file patent applications covering those inventions. It is also possible that others may have or may obtain issued patents that could prevent us from commercializing our products or require us to obtain licenses requiring the payment of significant fees or royalties in order to enable us to conduct our business. As to those patents that we may acquire, our continued rights will depend on meeting any obligations to the seller and we may be unable to do so. Our failure to obtain or maintain intellectual property rights for our inventions would lead to the loss of our investments in such activities, which would have a material adverse effect on us.

Moreover, patent application delays could cause delays in recognizing revenue from our internally generated patents and could cause us to miss opportunities to license patents before other competing technologies are developed or introduced into the market. We are not actively pursuing any commercialization opportunities or internally generated patents.

Our future success depends on our ability to expand our organization to match the growth of our activities.

As our operations grow, the administrative demands upon us will grow, and our success will depend upon our ability to meet those demands. We are organized as a holding company, with numerous subsidiaries. Both the parent company and each of our subsidiaries require certain financial, managerial and other resources, which could create challenges to our ability to successfully manage our subsidiaries and operations and impact our ability to assure compliance with our policies, practices and procedures. These demands include, but are not limited to, increased executive, accounting, management, legal services, staff support and general office services. We may need to hire additional qualified personnel to meet these demands, the cost and quality of which is dependent in part upon market factors outside of our control. Further, we will need to effectively manage the training and growth of our staff to maintain an efficient and effective workforce, and our failure to do so could adversely affect our business and operating results. Currently, we have limited personnel in our organization to meet our organizational and administrative demands. For example, we have reduced our workforce and have outsourced many services, including our accounting department.

Potential acquisitions may present risks, and we may be unable to achieve the financial or other goals intended at the time of any potential acquisition.

Our future growth may depend in part on our ability to acquire patented technologies, patent portfolios or companies holding such patented technologies and patent portfolios if we determine to again actively pursue patent monetization activities in the future. Such acquisitions are subject to numerous risks, including, but not limited to the following:

| ● | our inability to enter into a definitive agreement with respect to any potential acquisition, or if we are able to enter into such agreement, our inability to consummate the potential acquisition; | |

| ● | difficulty integrating the operations, technology and personnel of the acquired entity including achieving anticipated synergies; | |

| ● | our inability to achieve the anticipated financial and other benefits of the specific acquisition; | |

| ● | difficulty in maintaining controls, procedures and policies during the transition and monetization process; | |

| ● | diversion of our management’s attention from other business concerns; and | |

| ● | failure of our due diligence process to identify significant issues, including issues with respect to patented technologies and patent portfolios and other legal and financial contingencies. |

| 14 |

If we are unable to manage these risks effectively as part of any acquisition, our business could be adversely affected.

Our revenues are unpredictable, and this may harm our financial condition.

From November 12, 2012 to the present, our operating subsidiaries have executed our business strategy of acquiring patent portfolios and accompanying patent rights and monetizing the value of those assets. As of December 15, 2017, on a consolidated basis and taking into account the closing of the First Amendment and Restructuring Agreement with DBD, as further described herein, our operating subsidiaries owned 86 patents which include U.S. patents and certain foreign patents, covering technologies used in a wide variety of industries. Our revenues may vary substantially from quarter to quarter, which could make our business difficult to manage, adversely affect our business and operating results, cause our quarterly results to fall below expectations and adversely affect the market price of our Common Stock.

Our patent monetization cycle is lengthy and costly, and our marketing, legal and administrative efforts may be unsuccessful.

We expect significant marketing, legal and administrative expenses prior to generating revenue from monetization efforts. We will also spend considerable time and resources educating defendants on the benefits of a settlement, prior to or during litigation, that may include issuing a license to our patents and patent rights. As such, we may incur significant losses in any particular period before revenue streams commence.

If our efforts to convince defendants of the benefits of a settlement arrangement prior to litigation are unsuccessful, we may need to continue with the litigation process or other enforcement action to protect our patent rights and to realize revenue from those rights. We may also need to litigate to enforce the terms of existing license agreements, protect our trade secrets or determine the validity and scope of the proprietary rights of others. Enforcement proceedings are typically protracted and complex. The costs are typically substantial, and the outcomes are unpredictable. Enforcement actions will divert our managerial, technical, legal and financial resources from business operations.

Our exposure to uncontrollable risks, including new legislation, court rulings or actions by the United States Patent and Trademark Office), could adversely affect our activities including our revenues, expenses and results of operations.

Our patent acquisition and monetization business is subject to numerous risks including new legislation, regulations and rules. If new legislation, regulations or rules are implemented either by Congress, the United States Patent and Trademark Office, or USPTO, the executive branch, or the courts, that impact the patent application process, the patent enforcement process, the rights of patent holders, or litigation practices, such changes could materially and negatively affect our revenue and expenses and, therefore, our results of operations and the overall success of our Company. On March 16, 2013, the Leahy-Smith America Invents Act or the America Invents Act became effective. The America Invents Act includes a number of significant changes to U.S. patent law. In general, the legislation attempts to address issues surrounding the enforceability of patents and the increase in patent litigation by, among other things, establishing new procedures for patent litigation. For example, the America Invents Act changes the way that parties may be joined in patent infringement actions, increasing the likelihood that such actions will need to be brought against individual allegedly-infringing parties by their respective individual actions or activities. In addition, the America Invents Act enacted a new inter-partes review, or IPR, process at the USPTO which can be used by defendants, and other individuals and entities, to separately challenge the validity of any patent. These legislative changes, at this time, have had an impact on the costs and effectiveness of our patent monetization and enforcement business.

| 15 |

In addition, the U.S. Department of Justice, or the DOJ, has conducted reviews of the patent system to evaluate the impact of patent assertion entities on industries in which those patents relate. It is possible that the findings and recommendations of the DOJ could impact the ability to effectively monetize and enforce standards-essential patents and could increase the uncertainties and costs surrounding the enforcement of any such patented technologies. Also, the Federal Trade Commission, or FTC, has published its intent to initiate a proposed study under Section 6(b) of the Federal Trade Commission Act to evaluate the patent assertion practice and market impact of Patent Assertion Entities, or PAEs.

Finally, judicial rules regarding the burden of proof in patent enforcement actions could substantially increase the cost of our enforcement actions and new standards or limitations on liability for patent infringement could negatively impact our revenue derived from such enforcement actions.

The report of our independent registered public accounting firm expresses substantial doubt about Marathon’s ability to continue as a going concern.

Our auditors have indicated in their report on Marathon’s financial statements for the fiscal year ended December 31, 2016 that conditions exist that raise substantial doubt about our ability to continue as a going concern due to our recurring losses from operations and substantial decline in our working capital. A “going concern” opinion could impair our ability to finance our operations through the sale of equity, incurring debt, or other financing alternatives. If we are unable to continue as a going concern, we may have to liquidate our assets and may receive less than the value at which those assets are carried on our consolidated financial statements, and it is likely that investors will lose all or a part of their investment. We anticipate that our auditors for our 2017 fiscal year will also provide a “going concern” qualification in connection with their report.

Changes in patent laws could adversely impact our business.

Patent laws and judicial decisions or procedures may continue to change and may alter the historically consistent protections afforded to owners of patent rights. Such changes may not be advantageous for us and may make it more difficult for us to obtain adequate patent protection to enforce our patents against infringing parties. Increased focus on the growing number of patent-related lawsuits may result in legislative changes that increase our costs and related risks of asserting patent enforcement actions. For example, in May 2017, the United States Supreme Court reversed a ruling by a federal appeals court that handles patent cases, which had ruled since 1990 that suits could be filed essentially anywhere a business sold products, and held that patent suits should be filed in the state where the defendant is incorporated for patent infringement venue purposes. This could make it more difficult to seek damages for infringement.

Trial judges and juries often find it difficult to understand complex patent enforcement litigation, and as a result, we may need to appeal adverse decisions by lower courts in order to successfully enforce our patent rights.

It is difficult to predict the outcome of litigation, particularly patent enforcement litigation. It is often difficult for juries and trial judges to understand complex, patented technologies and, as a result, there is a higher rate of successful appeals in patent enforcement litigation than more standard business litigation. Such appeals are expensive and time consuming, resulting in increased costs and delayed final non-appealable judgments that can require payment of damages to Marathon. Although we diligently pursue enforcement litigation, we cannot predict with significant reliability the decisions that may be made by juries and trial courts.

| 16 |

More patent applications are filed each year resulting in longer delays in getting patents issued by the USPTO.

We hold and continue to acquire pending patents in the application or review phase. We believe there is a trend of increasing patent applications each year, which we believe is resulting in longer delays in obtaining approval of pending patent applications. The application delays could cause delays in monetizing such patents which could cause us to miss opportunities to license patents before other competing technologies are developed or introduced into the market.

The length of time required to litigate an enforcement action is increasing.

Our patent enforcement actions are almost exclusively prosecuted in federal court. Federal trial courts that hear our patent enforcement actions also hear criminal and other cases. Criminal cases always take priority over our actions. As a result, it is difficult to predict the length of time it will take to complete an enforcement action. Moreover, we believe there is a trend in increasing numbers of civil and criminal proceedings and, as a result, we believe that the risk of delays in our patent enforcement actions has grown and will continue to grow and will increasingly affect our business in the future unless this trend changes.

Any reductions in the funding of the USPTO could have an adverse impact on the cost of processing pending patent applications and the value of those pending patent applications.

Our ownership or acquisition of pending patent applications before the USPTO is subject to funding and other risks applicable to a government agency. The value of our patent portfolio is dependent, in part, on the issuance of patents in a timely manner, and any reductions in the funding of the USPTO could negatively impact the value of our assets. Further, reductions in funding from Congress could result in higher patent application filing and maintenance fees charged by the USPTO, causing an unexpected increase in our expenses.

Our acquisitions of patent assets may be time consuming, complex and costly, which could adversely affect our operating results.

Acquisitions of patent or other intellectual property assets, are often time consuming, complex and costly to consummate. We may utilize many different transaction structures in our acquisitions and the terms of such acquisition agreements tend to be heavily negotiated. As a result, we expect to incur significant operating expenses and may be required to raise capital during the negotiations even if the acquisition is ultimately not consummated. Even if we are able to acquire particular patent assets, there is no guarantee that we will generate sufficient revenue related to those patent assets to offset the acquisition costs. While we will seek to conduct sufficient due diligence on the patent assets we are considering for acquisition, we may acquire patent assets from a seller who does not have proper title to those assets. In those cases, we may be required to spend significant resources to defend our ownership interest in the patent assets and, if we are not successful, our acquisition may be invalid, in which case we could lose part or all of our investment in the assets.

We may also identify patent or other patent assets that cost more than we are prepared to spend. We may incur significant costs to organize and negotiate a structured acquisition that does not ultimately result in an acquisition of any patent assets or, if consummated, proves to be unprofitable for us. These higher costs could adversely affect our operating results and, if we incur losses, the value of our securities will decline.

In addition, we may acquire patents and technologies that are in the early stages of adoption in the commercial, industrial and consumer markets. Demand for some of these technologies will likely be untested and may be subject to fluctuation based upon the rate at which our companies may adopt our patented technologies in their products and services. As a result, there can be no assurance as to whether technologies we acquire or develop will have value that we can monetize.

| 17 |

In certain acquisitions of patent assets, we may seek to defer payment or finance a portion of the acquisition price. This approach may put us at a competitive disadvantage and could result in harm to our business.

We have limited capital and may seek to negotiate acquisitions of patent or other intellectual property assets where we can defer payments or finance a portion of the acquisition price. These types of debt financing or deferred payment arrangements may not be as attractive to sellers of patent assets as receiving the full purchase price for those assets in cash at the closing of the acquisition. As a result, we might not compete effectively against other companies in the market for acquiring patent assets, many of whom have substantially greater cash resources than we have. In addition, any failure to satisfy any debt repayment obligations that we may incur, may result in adverse consequences to our operating results.

Any failure to maintain or protect our patent assets could significantly impair our return on investment from such assets and harm our brand, our business and our operating results.

Our ability to operate our business and compete in the patent market largely depends on the superiority, uniqueness and value of our acquired patent assets. To protect our proprietary rights, we rely on and will rely on a combination of patent, trademark, copyright and trade secret laws, confidentiality agreements, common interest agreements and agreements with our employees and third parties, and protective contractual provisions. No assurances can be given that any of the measures we undertake to protect and maintain the value of our assets will be successful.

Following the acquisition of patent assets, we will likely be required to spend significant time and resources to maintain the effectiveness of such assets by paying maintenance fees and making filings with the USPTO. We may acquire patent assets, including patent applications that require us to spend resources to prosecute such patent applications with the USPTO. Moreover, there is a material risk that patent related claims (such as, for example, infringement claims (and/or claims for indemnification resulting therefrom), unenforceability claims or invalidity claims) will be asserted or prosecuted against us, and such assertions or prosecutions could materially and adversely affect our business. Regardless of whether any such claims are valid or can be successfully asserted, defending such claims could cause us to incur significant costs and could divert resources away from our core business activities.

Despite our efforts to protect our intellectual property rights, any of the following or similar occurrences may reduce the value of our intellectual property:

| ● | our patent applications, trademarks and copyrights may not be granted and, if granted, may be challenged or invalidated; | |

| ● | issued trademarks, copyrights, or patents may not provide us with any competitive advantages when compared to potentially infringing other properties; | |

| ● | our efforts to protect our intellectual property rights may not be effective in preventing misappropriation of our technology; or | |

| ● | our efforts may not prevent the development and design by others of products or technologies similar to or competitive with, or superior to those we acquire and/or prosecute. |

Moreover, we may not be able to effectively protect our intellectual property rights in certain foreign countries where we may do business in the future or from which competitors may operate. If we fail to maintain, defend or prosecute our patent assets properly, the value of those assets would be reduced or eliminated, and our business would be harmed.

| 18 |

We expect that we will be substantially dependent on a concentrated number of licensees. If we are unable to establish, maintain or replace our relationships with licensees and develop a diversified licensee base, our revenues may fluctuate, and our growth may be limited.

A significant portion of our patent monetization revenues will be generated from a limited number of licensees and licenses to such licensees. For the year ended December 31, 2016, the five largest licenses accounted for approximately 97% of our revenue. Some of these licenses were transferred to the SPE with DBD. There can be no guarantee that we will be able to obtain additional licenses for Marathon’s patents, or if we are able to do so, that the licenses will be of the same or larger size allowing us to sustain or grow our revenue levels, respectively. If we are not able to generate licenses from the limited group of prospective licensees that we anticipate may generate a substantial majority of our revenues in the future, or if they do not generate revenues at the levels or at the times that we anticipate, our ability to maintain or grow our revenues and our results of operations will be adversely affected.

Risks Related to Marathon’s Indebtedness

Our cash flows and capital resources may be insufficient to make required payments on our indebtedness and future indebtedness.

As of December 15, 2017, we have $4,053,948 of indebtedness outstanding. Our indebtedness could have important consequences to our shareholders. For example, it could:

| ● | make it difficult for us to satisfy our debt obligations; | |

| ● | make us more vulnerable to general adverse economic and industry conditions; | |

| ● | limit our ability to obtain additional financing for working capital, capital expenditures, acquisitions and other general corporate requirements; | |

| ● | expose us to interest rate fluctuations because the interest rate on the debt under our existing credit facility is variable; | |

| ● | require us to dedicate a portion of our cash flow from operations to payments on our debt, thereby reducing the availability of our cash flow for operations and other purposes; | |

| ● | limit our flexibility in planning for, or reacting to, changes in our business and the industry in which we operate; and | |

| ● | place us at a competitive disadvantage compared to competitors that may have proportionately less debt and greater financial resources. |

| 19 |

In addition, our ability to make payments or refinance our obligations depends on our successful financial and operating performance, cash flows and capital resources, which in turn depend upon prevailing economic conditions and certain financial, business and other factors, many of which are beyond our control. These factors include, among others:

| ● | economic and demand factors affecting our industry; | |

| ● | pricing pressures; | |

| ● | increased operating costs; | |

| ● | competitive conditions; and | |

| ● | other operating difficulties. |

If our cash flows and capital resources are insufficient to fund our debt service obligations, we may be forced to reduce or delay capital expenditures, sell material assets or operations, obtain additional capital or restructure our debt. In the event that we are required to dispose of material assets or operations to meet our debt service and other obligations, the value realized on such assets or operations will depend on market conditions and the availability of buyers. Accordingly, any such sale may not, among other things, be for a sufficient dollar amount. The foregoing encumbrances may limit our ability to dispose of material assets or operations. We also may not be able to restructure our indebtedness on favorable economic terms, if at all.

We may incur additional indebtedness in the future. Any incurrence of additional indebtedness would intensify the risks described above.

Risks Relating to Marathon’s Stock

Exercise or conversion of warrants and other convertible securities will dilute shareholder’s percentage of ownership.

We have issued convertible securities, options and warrants to purchase shares of our Common Stock to our officers, directors, consultants and certain shareholders. In the future, we may grant additional options, warrants and convertible securities. The exercise, conversion or exchange of options, warrants or convertible securities, including for other securities, will dilute the percentage ownership of our shareholders. The dilutive effect of the exercise or conversion of these securities may adversely affect our ability to obtain additional capital. The holders of these securities may be expected to exercise or convert such options, warrants and convertible securities at a time when we would be able to obtain additional equity capital on terms more favorable than such securities or when our Common Stock is trading at a price higher than the exercise or conversion price of the securities. The exercise or conversion of outstanding warrants, options and convertible securities will have a dilutive effect on the securities held by our shareholders. We have in the past, and may in the future, exchange outstanding securities for other securities on terms that are dilutive to the securities held by other shareholders not participating in such exchange.

| 20 |

Our Common Stock may be delisted from The NASDAQ Capital Market (“NASDAQ”) if we fail to comply with continued listing standards.

Our Common Stock is currently traded on NASDAQ under the symbol “MARA”. If we fail to meet any of the continued listing standards of NASDAQ, our Common Stock could be delisted from NASDAQ. We will be required to meet the more stringent requirements for an initial listing on NASDAQ in connection with the Merger in order for our Common Stock to continue to be listed on NASDAQ. During 2017 Marathon received multiple notices regarding failure to meet several continued listing standards, including $1.00 minimum closing bid price and $2.5 million stockholders’ equity requirements, which were subsequently satisfied. We have not held our 2017 annual meeting and, if an annual meeting is not held or an extension is not obtained from NASDAQ we will not be in compliance with the NASDAQ listing standards. Our repeated failures may impact our ability to continue to list our shares for trading on NASDAQ or to obtain approval of any initial listing application in connection with any acquisitions or other changes that require review and approval by NASDAQ. The continued listing standards include specifically enumerated criteria, such as:

| ● | a $1.00 minimum closing bid price; | |

| ● | stockholders’ equity of $2.5 million; | |

| ● | 500,000 shares of publicly-held Common Stock with a market value of at least $1 million; | |

| ● | 300 round-lot stockholders; and | |

| ● | compliance with NASDAQ’s corporate governance requirements, as well as additional or more stringent criteria that may be applied in the exercise of NASDAQ’s discretionary authority. |

The initial listing standards Marathon will be required to satisfy in order to obtain approval to continue to have its Common Stock approved for listing on The NASDAQ Capital Market following the closing of the Merger, in addition to satisfaction of NASDAQ’s corporate governance requirements and satisfaction of NASDAQ’s discretionary authority, will include:

| ● | $4 minimum closing bid price; | |

| ● | $4 or $5 million stockholders equity; | |

| ● | $5 or $15 million market value of publicly held shares; | |

| ● | 2 year operating history; | |

| ● | $50 million of market value of listed securities; | |

| ● | $750,000 of net income from continuing operations | |

| ● | 1 million publicly held shares; | |