10-K: Annual report [Section 13 and 15(d), not S-K Item 405]

Published on March 3, 2025

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark One)

For the fiscal year ended December 31 , 2024

or

For the transition period from _______to______

(Exact name of registrant as specified in charter)

|

(State or other jurisdiction

of incorporation or organization)

|

(Commission

File Number)

|

(I.R.S Employer

Identification No.)

|

||||||||||||

| (Address of principal executive offices) | (Zip Code) | |||||||

Registrant’s telephone number, including area code: 800 -804-1690

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | Trading Symbol(s) | Name of each exchange on which registered | ||||||||||||

The |

||||||||||||||

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act Yes ☒ No ☐

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Act. Yes ☐ No ☒

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes ☒ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| ☒ | Accelerated filer |

☐ | |||||||||

Non-accelerated filer |

☐ | Smaller reporting company |

|||||||||

| Emerging growth company | |||||||||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. ☒

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements. ☐

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant period pursuant to §240.10D-1(b). ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act) Yes ☐ No ☒

The aggregate market value of the common stock of the registrant held by non-affiliates was approximately $5.7 billion based on the closing sale price on The Nasdaq Capital Market on June 28, 2024 (the last business day of the registrant’s most recently completed second fiscal quarter).

As of February 21, 2025, the number of outstanding shares of the registrant’s common stock, par value $0.0001 per share, was 345,816,827 .

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the registrant’s Definitive Proxy Statement relating to the registrant’s 2025 annual meeting of stockholders, to be filed with the Securities and Exchange Commission within 120 days following the end of the fiscal year covered by this Annual Report on Form 10-K, are incorporated by reference in Part III within this Annual Report on Form 10-K. With the exception of the portions of the Proxy Statement specifically incorporated herein by reference, the Proxy Statement and related solicitation materials are not deemed to be filed as part of this Annual Report on Form 10-K.

TABLE OF CONTENTS

| Page | ||||||||

| Item 1. | ||||||||

| Item 1A. | ||||||||

| Item 1B. | ||||||||

| Item 1C. | ||||||||

| Item 2. | ||||||||

| Item 3. | ||||||||

| Item 4. | ||||||||

| Item 5. | ||||||||

| Item 6. | ||||||||

| Item 7. | ||||||||

| Item 7A. | ||||||||

| Item 8. |

F-1

|

|||||||

| Item 9. | ||||||||

| Item 9A. | ||||||||

| Item 9B. | ||||||||

| Item 9C. | ||||||||

| Item 10. | ||||||||

| Item 11. | ||||||||

| Item 12. | ||||||||

| Item 13. | ||||||||

| Item 14. | ||||||||

| Item 15. | ||||||||

| Item 16. | ||||||||

MARA HOLDINGS, INC.

As used in this Annual Report on Form 10-K for our fiscal year ended December 31, 2024 (this “Annual Report”), the terms the “Company,” “MARA,” “we,” “our” and “us” refer to MARA Holdings, Inc. (f/k/a Marathon Digital Holdings, Inc.) and its subsidiaries, unless otherwise indicated.

CAUTIONARY NOTE REGARDING FORWARD-LOOKING STATEMENTS

Some of the statements under “Business,” “Risk Factors,” “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and elsewhere in this Annual Report may contain forward-looking statements that reflect our current views with respect to, among other things, future events, results and financial performance, which are intended to be covered by the safe harbor provisions for forward-looking statements provided by the Private Securities Litigation Reform Act of 1995.

These statements can be identified by the fact that they do not relate strictly to historical or current facts, and you can often identify these forward-looking statements by the use of forward-looking words such as “anticipate,” “believe,” “contemplate,” “continue,” “could,” “estimate,” “expect,” “forecast,” “goal,” “intend,” “may,” “outlook,” “plan,” “potential,” “predict,” “project,” “seek,” “shall,” “should,” “strive,” “target,” “will” or the negative version of those words or other comparable words. Any forward-looking statements contained in this Annual Report are based upon our historical performance and on our current plans, estimates and expectations in light of information currently available to us. The inclusion of this forward-looking information should not be regarded as a representation by us that the future plans, estimates or expectations contemplated by us will be achieved. Such forward-looking statements are subject to various risks and uncertainties and assumptions relating to our operations, financial results, financial condition, business, prospects, growth strategy and liquidity. Accordingly, there are or will be important factors that could cause our actual results to differ materially from those indicated in these statements. You should not place undue reliance on any forward-looking statements and should consider the factors discussed under “Risk Factors” in Part I, Item 1A herein.

The factors identified in Part I, Item 1A herein should not be construed as an exhaustive list of factors that could affect our future results and should be read in conjunction with the other cautionary statements that are included in this Annual Report. The forward-looking statements made in this Annual Report are made only as of the date of this Annual Report. We do not undertake any obligation to publicly update or review any forward-looking statement except as required by law, whether as a result of new information, future developments or otherwise.

If one or more of these or other risks or uncertainties materialize, or if our underlying assumptions prove to be incorrect, our actual results may vary materially from what we may have expressed or implied by these forward-looking statements. You should specifically consider the factors identified in this Annual Report that could cause actual results to differ before making an investment decision to purchase our common stock.

Furthermore, new risks and uncertainties arise from time to time, and it is impossible for us to predict those events or how they may affect us.

5

PART I

ITEM 1. BUSINESS

CORPORATE OVERVIEW

MARA is a global leader in leveraging digital asset compute to support the energy transformation, with operations on four continents and 16 data centers in North America, the Middle East, Europe and Latin America. We employ different strategies and structures (self-owned, joint ventures, and third-party hosted) to diversify risk across the organization. In prior years, we primarily used third party hosted sites to operate with an asset-light model. During the year, we decided to diversify our portfolio of assets and increased the proportion of our owned mining sites, exiting the year at approximately 70% owned capacity. Our core business is bitcoin mining, and we produce, or “mine,” bitcoin using one of the industry’s largest and most energy-efficient fleets of specialized computers while providing dispatchable compute as an optionality to the electric grid operators to balance electric demands on the grid.

We are exploring low cost energy initiatives through our owned power generation business, which focuses on disintermediating pipelines and powerlines by locating operations directly at energy sources, such as renewable energy sites and methane gas capture locations. Over time, it is our expectation that this strategy will reduce production costs, improve operating margins, lower the weighted average cost of capital, and extend the duration of our bitcoin mining rigs and capacity. Our low cost energy strategy focuses on reducing costs by utilizing stranded energy and exploring other opportunities, including selling excess capacity to offset costs and pursuing revenue generating initiatives that provide higher margins, thereby reducing our reliance on higher electricity costs. For example, subsequent to year end, we acquired an electric generating wind farm facility to utilize last-generation bitcoin mining rigs to provide an avenue for the hardware to continue operating profitably beyond its normal lifecycle.

In addition, we are expanding our involvement in complementary businesses that align with our core competencies and strategic goals. This includes the sale of data center infrastructure, such as immersion-cooled systems, to third parties operating in the bitcoin ecosystem and the artificial intelligence (“AI”) and high-performance compute (“HPC”) sector. Our business is also active in bitcoin-related projects focused on the technological development of immersion, hardware, firmware, mining pools and side chains that leverage blockchain cryptography.

We believe we are the second largest holder of bitcoin among publicly traded companies. From time to time, we enter into forward or option contracts and/or lend bitcoin to increase yield on our bitcoin holdings.

As used throughout this Annual Report, the term “Bitcoin” with a capital “B” is used to denote the Bitcoin protocol which implements a highly available, public, permanent, and decentralized ledger. The terms “bitcoin” with a lower case “b” and “BTC” are used to denote the coin, bitcoin.

BITCOIN BLOCKCHAIN

Bitcoin and Bitcoin Mining

Bitcoin is a decentralized digital asset that operates on a peer-to-peer network, allowing users to send and receive payments without the need for banks and other intermediaries. Bitcoin is not linked to any fiat currency or country’s monetary policy and therefore serves as a store of value outside of government control. This is possible by using blockchain technology, which is a distributed ledger that records and verifies all transactions on the network.

The Bitcoin blockchain is a public, transparent, and unalterable record of all transactions that have ever occurred on the peer-to-peer network. When a user sends a transaction on the Bitcoin network, it is broadcast to the network and added to a pool of unconfirmed transactions known as the “mempool.” Miners, which operate specialized hardware, known as bitcoin mining rigs or application-specific integrated circuits (“ASICs”), then compete to process these unconfirmed transactions into a “block.” The first miner to successfully confirm and assemble the transactions into a block receives a reward in the form of newly minted bitcoin (block subsidy) and transaction fees. Each confirmed transaction is cryptographically signed and permanently recorded in the blockchain as a new block, and cannot be altered or deleted.

6

The blockchain is maintained by a robust and public open-source architecture consisting of a network of computers, known as nodes, that work together to verify and validate new transactions. Because the blockchain is decentralized and transparent, all users can verify the legitimacy of a transaction without having to rely on a third party. This eliminates the need for intermediaries, which can be slow and expensive, and makes the network resistant to censorship and fraud.

Bitcoin mining plays a key role in the maintenance and growth of the Bitcoin network by providing the computational power needed to verify transactions and add new blocks to the blockchain. We believe that, as the Bitcoin network becomes more secure, its enhanced security may drive greater adoption and transaction volumes and fees.

As of December 31, 2024, we operated approximately 400,000 mining rigs globally, with an energized hashrate of approximately 53.2 exahashes per second (“EH/s”). During the year ended December 31, 2024, we mined 9,430 bitcoin. We remain focused on maximizing our chances of successfully processing blocks on the Bitcoin blockchain by growing our hashrate, or the amount of computational power we devote to supporting the Bitcoin blockchain, to enhance our ability to successfully process blocks. Generally, the greater the share a single miner can capture of the blockchain’s total network hashrate, or the aggregate hashrate deployed to processing blocks on the Bitcoin blockchain, the greater the miner’s chances of processing a block and therefore earning the reward. As additional mining operators enter the market in response to increased demand for bitcoin, the Bitcoin blockchain’s network hashrate grows.

Bitcoin “Halving” Events

Bitcoin halving is a phenomenon that has historically occurred every 210,000 blocks or approximately every four years on the Bitcoin network. The halving is a key part of the Bitcoin protocol and serves to control the overall supply and reduce the risk of inflation in digital assets using a Proof-of-Work consensus algorithm. At a predetermined block, the block subsidy portion of the reward is cut in half, hence the term “halving.” For example, the block subsidy for adding a single block to the blockchain was initially set at 50 bitcoin currency rewards. The Bitcoin blockchain has undergone a halving four times since its inception, most recently in April 2024. The next halving for the Bitcoin blockchain is anticipated to occur around April 2028. This process will recur until the total amount of bitcoin currency rewards issued reaches 21,000,000, and the theoretical supply of new bitcoin is exhausted, which is expected to occur around 2140. Many factors influence the price of Bitcoin, and potential increase or decrease in prices in advance of or following the future halving is unknown.

At the beginning of the year, the reward for each solved block was equal to 6.25 bitcoin plus transaction fees. On April 19, 2024, the bitcoin halving event occurred, reducing the previous block reward to 3.125 bitcoin per block. The transaction fee was not impacted by the halving.

As of December 31, 2024, the price of bitcoin was $93,354.

Factors Affecting Profitability

Market Price of Bitcoin

Our business is heavily dependent on the price of bitcoin. The prices of digital assets, including bitcoin, have historically experienced substantial volatility, and digital asset prices have in the past and may in the future be driven by speculation and incomplete information, subject to rapidly changing investor sentiment, and influenced by factors such as technology, macroeconomic conditions, regulatory void or changes, fraudulent actors, manipulation, and media reporting. Further, the value of bitcoin and other digital assets may be significantly impacted by factors beyond our control, including consumer trust in the market acceptance of bitcoin as a means of exchange by consumers and merchants.

7

Halving

The halving is an important part of the Bitcoin ecosystem, and it is closely watched by miners, investors, and other participants in the digital asset market. Each halving event has historically been associated with significant price movements in the value of bitcoin.

Network Hashrate and Difficulty

Generally, a bitcoin mining rig’s chance of solving a block on the Bitcoin blockchain and earning a bitcoin reward is a function of the mining rig’s hashrate, relative to the global network hashrate (i.e., the aggregate amount of computing power devoted to supporting the Bitcoin blockchain at a given time). As demand for bitcoin increases, the global network hashrate rapidly increases, and as more adoption of bitcoin occurs, we expect the demand for new bitcoin will likewise increase as more mining companies are drawn into the industry by this increase in demand. Further, as more and increasingly powerful mining rigs are deployed, the network difficulty for Bitcoin increases. Network difficulty is a measure of how difficult it is to solve a block on the Bitcoin blockchain, which is adjusted every 2,016 blocks, or approximately every two weeks, so that the average time between each block is approximately ten minutes. A high difficulty means that it will take more computing power to solve a block and earn a new bitcoin reward, which, in turn, makes the Bitcoin network more secure by limiting the possibility of one miner or mining pool gaining control of the network. Therefore, as new and existing miners deploy additional hashrate, the global network hashrate will continue to increase, meaning a miner’s share of the global network hashrate (and therefore its chance of earning bitcoin rewards) will decline if it fails to deploy additional hashrate at pace with the industry.

STRATEGIC FOCUS

Our focus in 2024 was on growth, execution and transition into a more mature organization with a diversified portfolio of bitcoin mining sites while strategically reducing bitcoin production costs. This focus consisted of the expansion of operations of our core bitcoin mining business, acquiring and operating bitcoin mining sites to host our own bitcoin mining rigs and deploying low cost energy initiatives. Key activities and milestones during 2024 included the following:

•We more than doubled our hashrate to 53.2 EH/s.

•We acquired five operational data centers, totaling 812 megawatts (“MW”) of nameplate capacity, in Granbury and Garden City, Texas, Kearney, Nebraska, and Hannibal and Hopedale, Ohio.

•We entered into an agreement to acquire a wind farm in Hansford County, Texas, with 240 MW of interconnection capacity and 114 MW of nameplate wind capacity to establish a behind-the-meter data center at low energy costs and provide an avenue for prior-generation bitcoin mining rigs to continue operating profitably beyond their normal lifecycle. The acquisition closed subsequent to year end.

•We launched a 25 MW micro data center operation in partnership with an oil and gas company, utilizing excess, flared natural gas from oil wellheads in Texas and North Dakota to power our bitcoin mining operations. This operation mitigates up to 99% of methane emissions and drives down our energy costs.

•In Finland, we deployed two pilot projects to recycle heat from our operations, providing heat to communities with a total population of approximately 80,000 residents. These sites offset our production costs through heat sales while reducing the local communities’ reliance on high carbon emitting biomass through the use of hydro power, delivering renewable energy and more affordable heating to communities.

•We launched a program to generate additional return by loaning bitcoin. At year end, we had approximately 10,374 bitcoin under loaned or collateral arrangements.

•We grew bitcoin holdings (including loaned and collateralized bitcoin) by 197% to 44,893, which highlights our commitment to our core operations while also recognizing opportunities to purchase bitcoin strategically.

8

Our primary focus in 2025 is to keep our current fleet of over 400,000 bitcoin mining rigs energized and running optimally while increasing our total hashrate. We anticipate further growth of our hashrate in 2025 as we bring newly acquired bitcoin miners into operation.

We have grown quickly to become a global leader in leveraging digital asset compute to support energy transformation. We achieved this milestone through an asset-heavy strategy, which involved deploying our bitcoin miners at third-party hosted sites and making strategic acquisitions throughout 2024. During the year ended December 31, 2024 we announced a significant shift in our treasury policy and adopted a full holding onto bitcoin (“HODL”) strategy to retain all mined and purchased bitcoin for the foreseeable future. The adoption of this strategy reflects our confidence in the long-term value of bitcoin and our belief that it is the world’s best treasury reserve asset.

In addition to this approach, we implemented a hybrid bitcoin acquisition strategy, balancing mining with opportunistic market purchases, leveraging approximately $2.2 billion in aggregate principal amount of convertible senior notes (the “2024 Convertible Notes”), of which $1.9 billion bears no interest. In 2024, we acquired 22,065 bitcoin at an average price of $87,205 and mined an additional 9,430 bitcoin, increasing our total bitcoin holdings to 44,893 as of December 31, 2024. These holdings were valued at approximately $4.2 billion based on a spot price of $93,354 per bitcoin on of December 31, 2024, strengthening our liquidity position – a priority that we intend to continue focusing on in 2025.

As of December 31, 2024, we had approximately 7,377 bitcoin loaned to third parties, generating yield from our loaned bitcoin, and approximately 2,997 bitcoin utilized as collateral for borrowings. Our combined cash and cash equivalents, excluding restricted cash and digital assets, including loaned and collateralized bitcoin, totaled nearly $4.6 billion as of December 31, 2024. Refer to Part II, Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations, “Financial Condition and Liquidity” included in this Annual Report for further information.

We also expect to deploy several technological innovations developed by our technology team and partners at our operations and bring them to market. These innovations include a new two-phase immersion-cooling (“2PIC”) system, designed to optimize cooling efficiency, mining rig performance, and heat capture and reuse, as well as new hardware and software solutions. Deployments of 2PIC technology have already begun, with tanks scheduled for integration across key sites to improve both our operations and those of external customers. Initially, we expect to be the primary user of 2PIC.

Research and Development

Our research and development (“R&D”) efforts play a critical role in driving our innovation and growth. Our R&D process is designed to support the creation and development of new tools and processes intended to serve an integral part of our overall business strategy and enhance our market position as an advanced and sustainable bitcoin miner. Additionally, R&D includes activities related to AI and adjacent markets, with the goal of creating additional revenue opportunities over the long term.

The first step in the R&D process is ideation, which is the process of generating and evaluating new ideas. We encourage our team members to come up with creative and innovative ideas, and then we provide them with the resources and support they need to explore these ideas further.

Once we have identified a promising idea, the next step is to develop a prototype. This typically involves creating a small-scale version of the product or service, which can be tested and evaluated in order to identify potential issues and improve the design. We conduct market research to understand the potential market for the product or service.

The final step in our R&D process is testing and validation. This involves conducting thorough testing of the prototype to identify any issues or flaws, and to ensure that it meets our rigorous quality standards. We also conduct market testing to gather feedback from real-world users, and use this feedback to refine and improve the product or service.

9

Overall, our R&D process is designed to support the creation and development of innovative technology advancements that ensure we maintain our competitive advantages and improve our position as a leading bitcoin miner. We believe that this process is essential for driving growth, staying ahead of the competition, and achieving success.

Strategic Investments

We are committed to pursuing strategic investments that align with our vision and values. Our strategic focus is to identify and partner with companies that we believe will generate synergies to create long-term value for our stockholders.

A core element of our investment strategy is to focus on companies that are at the forefront of emerging technologies and industries. We believe targeted companies have the potential to drive significant innovation and growth, and we are committed to supporting the development through investments in both hardware and software companies.

Another key aspect of our strategy is to prioritize investments in companies that are aligned with our values and mission. We believe our stockholders expect us to support businesses that operate in a responsible and sustainable manner, and we are committed to making investments that reflect these values.

Overall, our investment strategy is designed to support our growth and success, while propelling our business to be the most advanced, agile, and efficient bitcoin miner. We are committed to making strategic investments that align with both our vision and values, and believe this approach will help us achieve long-term success.

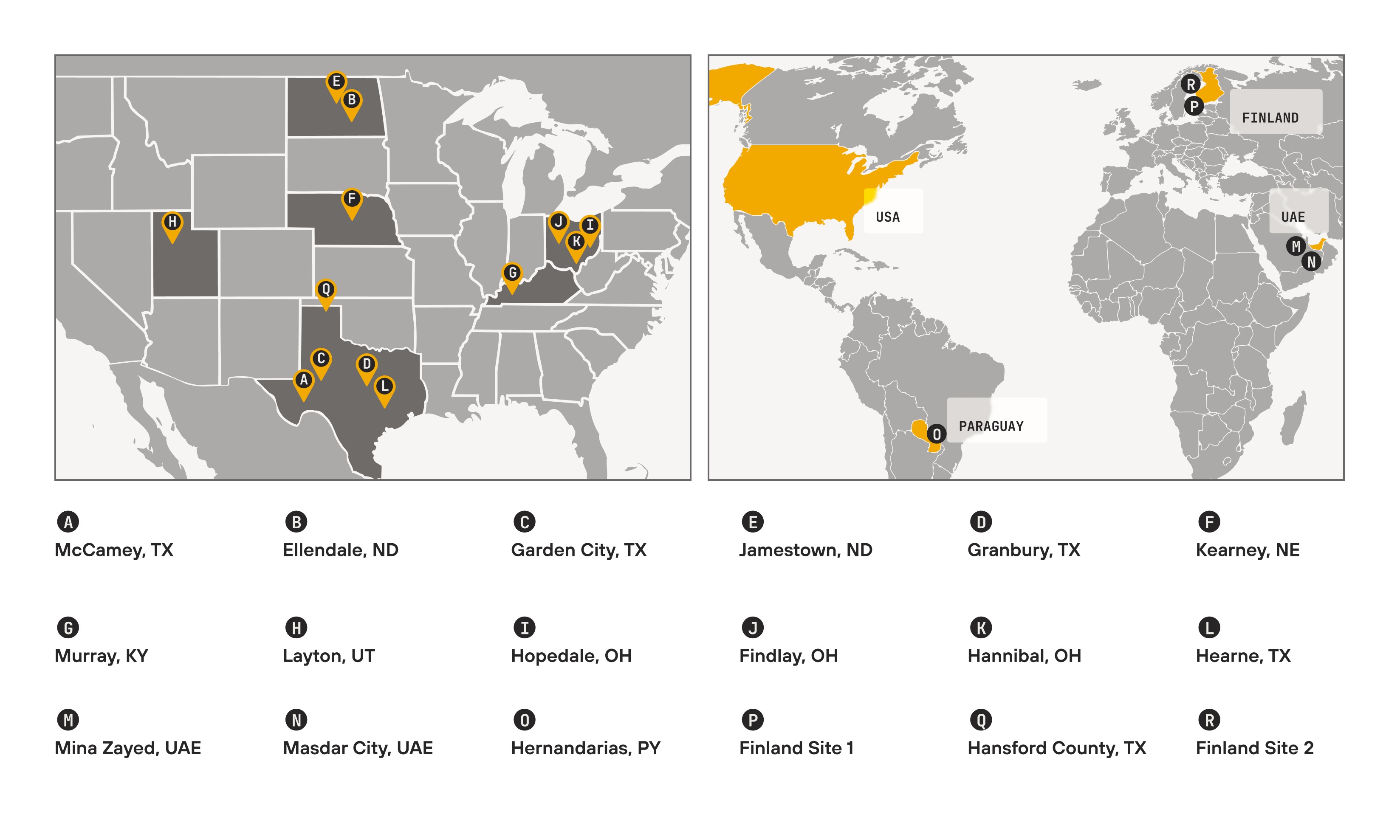

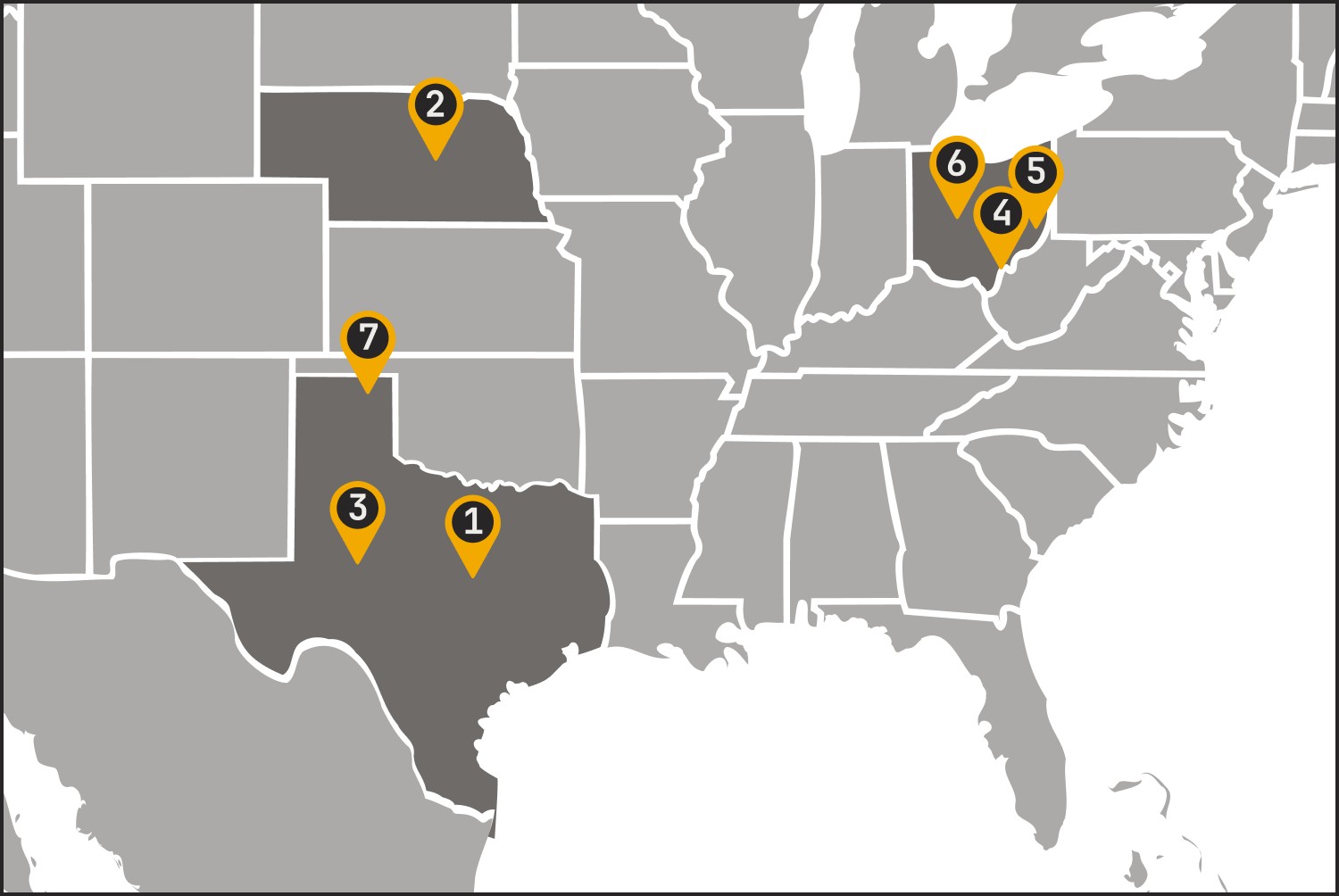

OPERATIONS

We deploy miners at sites on four continents. The following map and table represent our site locations and provide current megawatt (“megawatt” or “MW”) and exahash capacity and expansion opportunities:

10

Site Location |

Type |

Operational Capacity (MW) |

Growth Capacity (MW) (1)

|

Total Nameplate Capacity (MW) |

Energized Exahash | |||||||||||||||||||||||||||

Owned Sites |

||||||||||||||||||||||||||||||||

| Granbury, Texas | Colocated generation + grid | 232 | 68 | 300 | 12.1 | |||||||||||||||||||||||||||

| Garden City, Texas | Colocated generation + grid | 126 | 74 | 200 | 8.2 | |||||||||||||||||||||||||||

| Hannibal, Ohio | Grid connection | 41 | 159 | 200 | — | |||||||||||||||||||||||||||

Hansford County, Texas (2)

|

Colocated with wind generation | — | 180 | 180 | — | |||||||||||||||||||||||||||

| Findlay, Ohio | Grid connection | 26 | 124 | 150 | 1.2 | |||||||||||||||||||||||||||

| Kearney, Nebraska | Grid connection | 92 | 8 | 100 | 5.8 | |||||||||||||||||||||||||||

| Hopedale, Ohio | Grid connection | 21 | 4 | 25 | 0.9 | |||||||||||||||||||||||||||

| Hearne, Texas | Flare gas | 22 | — | 22 | 0.6 | |||||||||||||||||||||||||||

| International | Various | 57 | — | 57 | 2.1 | |||||||||||||||||||||||||||

| Total Owned Sites | 617 | 617 | 1,234 | 30.8 | ||||||||||||||||||||||||||||

Hosted Sites |

||||||||||||||||||||||||||||||||

| McCamey, Texas | Colocated generation + grid | 216 | — | 216 | 7.6 | |||||||||||||||||||||||||||

| Ellendale, North Dakota | Grid connection | 180 | — | 180 | 10.5 | |||||||||||||||||||||||||||

| Jamestown, North Dakota | Grid connection | 93 | — | 93 | 3.7 | |||||||||||||||||||||||||||

| Other | Various | 12 | — | 12 | 0.6 | |||||||||||||||||||||||||||

| Total Hosted Sites | 501 | — | 501 | 22.4 | ||||||||||||||||||||||||||||

| Total | 1,118 | 617 | 1,735 | 53.2 | ||||||||||||||||||||||||||||

(1) Subject to certain utility approval, interconnection studies, land lease/acquisitions and/or regulatory approvals.

(2) The Hansford County, Texas acquisition closed subsequent to year end, on February 14, 2025.

COMPETITION

In digital asset mining, companies and individuals use computing power to solve cryptographic algorithms to record and publish transactions to blockchain ledgers or provide transaction verification services to the Bitcoin network in exchange for digital asset rewards. The current reward for verifying a block on the Bitcoin blockchain is 3.125 bitcoin. Miners can range from individual enthusiasts to professional mining operators with dedicated data centers. Miners may organize themselves in mining pools. We compete or may in the future compete with other companies that focus all or a portion of their activities on owning or operating digital asset exchanges, developing programming for the blockchain, and mining activities. Currently, the information concerning the activities of these enterprises is not readily available as the vast majority of the participants in this sector do not publish information publicly or the information may be unreliable.

We believe our acquisitions and our ongoing deployment of miners positions us well among the publicly traded companies involved in the digital asset mining industry. The digital asset mining industry is a highly competitive and evolving industry and new competitors and/or emerging technologies could enter the market and affect our competitiveness in the future.

11

INTELLECTUAL PROPERTY

We actively use specific hardware and software for digital asset mining operations. In certain cases, source code and other software assets may be subject to an open-source license, as much of the technology development underway in our sector is open source.

We currently own two patents in the United States and have 17 patent applications pending. Our patents have various expiration dates, generally 20 years from the respective original filing date. Our patents improve efficiency to decrease settlement risk and expand server and radio functionalities. In the future, we may seek to register additional patents in connection with our existing and planned blockchain and digital asset operations.

To protect and enforce our proprietary information and intellectual property, we rely upon trade secrets, trademarks, service marks, trade names, copyrights and other intellectual property rights.

Additionally, we expect to continue to license the use of intellectual property rights owned and controlled by others. We also have developed, and may further develop, certain proprietary software applications for purposes of our digital asset mining operations and may license proprietary software application to third parties.

REGULATORY LANDSCAPE

We operate within a complex and rapidly evolving regulatory environment and are subject to a wide range of laws and regulations enacted by U.S. federal, state, and local governments, governmental agencies, and regulatory authorities, including the U.S. Securities and Exchange Commission (the “SEC”), the Commodity Futures Trading Commission (the “CFTC”), the Federal Trade Commission (the “FTC”), and the Financial Crimes Enforcement network of the U.S. Department of Treasury, as well as similar entities in other countries. Other regulatory bodies have demonstrated an interest in regulating or investigating companies engaged in blockchain or cryptocurrency businesses.

Regulations may substantially change in the future and it is presently not possible to know how regulations will apply to our business, or when they may be effective. While we anticipate that bitcoin mining will be an area of focus for regulators in 2025 and beyond, we cannot predict with certainty the impact regulations may have on our business or operations. As the regulatory and legal environment evolves, we may become subject to new laws and regulations by the SEC and other agencies, which may affect our mining operations and other activities. Additionally, state and local regulation of bitcoin mining is important with respect to where we conduct our mining operations. A substantial number of our bitcoin miners are located in Texas and North Dakota, which are generally favorable regulatory environments for bitcoin miners compared to other states. However, we may also become subject to additional regulatory requirements on a state and local level in the geographies in which we operate, and as we strategically expand our operations into new areas.

For additional discussion of potential risks that existing and future regulation may pose to our business, see Part I, Item 1A. “Risk Factors” of this Annual Report.

HUMAN CAPITAL RESOURCES

As of December 31, 2024, we had a total workforce of approximately 152 employees across our entire organization, all of whom were employed full-time, including professionals in accounting, communications, engineering, finance, growth, human resources, information and technology, investor relations, legal and operations.

Our human capital resources strategy is to align the interests of our employees with our key long-term success drivers. In execution of this strategy, we maintain an equity incentive plan, under which all eligible employees can receive equity grants. We believe our equity plan serves as a key incentive for our employees, aligning their long-term interests with our objectives as an organization.

12

We also compare salary and wages against quantitative benchmarks and adjust monetary compensation to ensure wages are competitive and consistent with employee positions, skill levels, experience, and geographic location. We maintain a robust process for ensuring pay equity across MARA and increases in incentives and compensation based on merit and performance. In addition, we provide a comprehensive range of benefits options, including medical, dental and vision insurance for employees and family members, paid and unpaid leaves, and life and disability/accident coverage.

At MARA, we seek to attract a pool of diverse, best-in-class candidates and foster their career growth by hiring the best talent available, rather than relying solely on educational background. In support of such initiative, we look for candidates in local communities and large cities alike, and from a variety of backgrounds. Our goal is a long-term, growth-oriented career for each employee. We also believe that our ability to retain our workforce is dependent on our ability to foster an environment that is sustainably safe, respectful, fair, and inclusive of everyone.

CORPORATE HISTORY AND AVAILABLE INFORMATION

Previously known as Marathon Digital Holdings, Inc., we changed our name to MARA Holdings, Inc. on August 29, 2024.

Our website address is www.mara.com. The information contained on or connected to our website is not incorporated by reference into this Annual Report and should not be considered part of this or any other report filed with the SEC. Our annual reports on Form 10-K, quarterly reports on Form 10-Q and current reports on Form 8-K, as well as any amendments to those reports, are available free of charge through our website as soon as reasonably practicable after we file them with, or furnish them to, the SEC.

ITEM 1A. RISK FACTORS

Described below are certain risks to our business and the industry in which we operate. You should carefully consider the risks described below, together with the financial and other information contained in this Annual Report and in our other public disclosures. If any of the following risks actually occurs, our business, financial condition, results of operations, cash flows and prospects could be materially and adversely affected. As a result, our future results could differ materially from historical results and from guidance we may provide regarding our expectations of our future financial performance, and the trading price of our common stock could decline.

Risk Factors Summary

The following is a summary of the principal factors that make an investment in our securities speculative or risky, all of which are more fully described below in this section. This summary should be read in conjunction with the full description of “Risk Factors” in this section and should not be relied upon as an exhaustive summary of the material risks facing our business. In addition to the following summary and the information in this section, you should consider the other information contained in this Annual Report before investing in our securities.

Risks Related to Our Business

•Bitcoin price volatility may affect our ability to effectively manage our growth plans and profitability;

•Regulatory, commercial, and technical uncertainties may influence bitcoin prices;

•Failure to increase our hashrate may reduce our competitiveness and negatively impact our financial performance;

•Our HODL strategy exposes us to market volatility and liquidity risks;

•Significant disruptions in the cryptocurrency markets, like those in late 2022, could materially impair the value of our mining rigs, and prolonged low bitcoin prices could force us to idle mining rigs;

•The adoption and long-term viability of digital asset networks is uncertain, and a decline in their growth or acceptance could negatively impact our business and the value of our stock;

•We face risks related to technological obsolescence, vulnerability of the global supply chain for cryptocurrency hardware, potential trade restrictions and difficulty in obtaining new hardware, which may have a material adverse effect on our business;

13

•We may experience liquidity constraints and need additional capital, which may not be available to us on favorable terms, or at all;

•Our bitcoin lending arrangements expose us to risks of borrower default, operational failures and cybersecurity threats;

•The U.S. political and economic environment could materially impact our business operations and financial performance, and uncertainty surrounding the potential legal, regulatory and policy changes by the new U.S. presidential administration may directly affect us and the global economy;

•We have engaged in, and may continue to engage in, strategic acquisitions and other transactions that could disrupt our business, dilute our stockholders, strain our financial resources and harm our operating results;

•Geopolitical and economic crises could lead to increased uncertainty, large-scale selloffs of digital assets and a decline in bitcoin’s value, negatively impacting our business and stock price; and

•The lack of legal recourse and insurance for our digital assets increases the risk of total loss in the event of theft or destruction.

Risks Related to Governmental Regulation and Enforcement

•The rapidly evolving and uncertain regulatory landscape for cryptocurrencies exposes us to legal risks, compliance costs, and potential business disruptions;

•The unregulated nature and lack of transparency of many bitcoin trading venues may expose us to fraud, security failures, and operational risks, potentially harming the value of our bitcoin holdings;

•If bitcoin is classified as a security, we may be subject to extensive regulation, which could result in significant costs or force us to cease certain operations;

•Our bitcoin holdings could subject us to regulatory scrutiny and potential restrictions on future transactions;

•Operating in foreign jurisdictions exposes us to political, legal, and regulatory risks that could negatively impact our financial condition; and

•Target energy regulations and taxes could increase our costs and adversely affect our business.

Risks Related to Our Common Stock

•Our stock price is volatile and subject to significant fluctuations;

•Our ongoing at-the-market stock issuances contribute to stockholder dilution and may intensify due to our HODL strategy;

•The issuance, conversion, or exercise of convertible notes and other convertible securities, options, and warrants will dilute our stockholders’ ownership; and

•Uncertainty in accounting standards for bitcoin and other cryptocurrencies may lead to financial restatements and business disruptions.

Risks Related to Our Business

Bitcoin price volatility may affect our ability to effectively manage our growth plans and profitability.

The market price of bitcoin is extremely volatile, and in fiscal 2024 the price range of bitcoin was between approximately $39,000 and $106,000. The cost to mine a bitcoin is independent of the then current price of bitcoin, so when bitcoin prices are low, the cost per coin to mine may consume much of our available cash, limiting our ability to invest in expansion, upgrade mining equipment and infrastructure or fund other strategic initiatives. Additionally, because our revenue is primarily derived from mining bitcoin, our profitability fluctuates in direct correlation with bitcoin price movements. A decrease in bitcoin’s price results in a corresponding decrease in the value of the bitcoin we mine, reducing our revenues and profitability on a dollar-for-dollar basis. Given the volatility of bitcoin prices, we are unable to accurately predict our future growth trajectory or reliably forecast our revenue and profitability for any given reporting period. Our ability to expand our operations depends on our assumptions regarding bitcoin’s future price. If those assumptions are incorrect, and bitcoin prices fail to reach or sustain levels

14

high enough to justify our capital expenditures, we may be unable to generate sufficient revenue to maintain profitability or execute our growth strategy, which could materially and adversely impact our business, financial condition and results of operations.

Regulatory, commercial and technical uncertainties may influence bitcoin prices.

The market price of bitcoin is subject to numerous uncertainties, including evolving regulatory frameworks, commercial adoption trends and technical risks, any of which could negatively impact its value. Regulatory treatment of digital assets remains uncertain in various jurisdictions, and new regulations, enforcement actions, or interpretations by governmental authorities could diminish bitcoin’s appeal, restrict its use or otherwise depress its market price.

Beyond regulation, bitcoin’s price is influenced by factors such as:

•public perception and media coverage of bitcoin and digital assets;

•accessibility and convenience of purchasing, holding and transacting with bitcoin;

•institutional demand for bitcoin as an asset class;

•consumer adoption of bitcoin for everyday transactions; and

•emergence of competing digital assets with potentially superior functionality, scalability or regulatory compliance.

Even if bitcoin adoption increases in the short term, there is no guarantee that this growth will be sustained. Since bitcoin exists solely as digital records on the Bitcoin blockchain, its value is also susceptible to technical risks, including:

•a decrease in miner incentives due to declining block rewards and transaction fees;

•security vulnerabilities, such as potential network attacks or software exploits;

•forks or changes to the Bitcoin protocol that may split the network or cause instability; and

•developments in mathematics or technology, including in digital computing, algebraic geometry and quantum computing, that could result in the cryptography used by the Bitcoin blockchain becoming insecure or ineffective.

Additionally, bitcoin’s liquidity could be adversely affected if financial institutions, payment processors or market makers withdraw their support for bitcoin-related services due to regulatory pressure, reputational concerns or operational risks. If any of these risks materialize, they could negatively impact bitcoin’s market price, which, in turn, would adversely affect our business and financial condition.

Failure to increase our hashrate may reduce our competitiveness and negatively impact our financial performance.

Our ability to earn bitcoin rewards is directly proportional to our mining power, or hashrate, relative to the total hashrate of the Bitcoin network. As more miners enter the network and deploy more powerful mining equipment, the global hashrate increases, making it more difficult to successfully mine bitcoin. To remain competitive, we must continuously invest in expanding our hashrate by acquiring new, more efficient mining hardware. However, as demand for mining equipment grows, the cost of acquiring and deploying new miners increases, which could limit our ability to scale. If we are unable to access capital to acquire additional miners, our hashrate may stagnate and we may fall behind our competitors. If we fail to increase our hashrate at a pace that keeps up with network difficulty growth, our share of total bitcoin mining rewards will decline, reducing our revenue and negatively impacting our financial performance.

Our HODL strategy exposes us to market volatility and liquidity risks.

In the third quarter of 2024, we adopted a HODL strategy whereby we retain all bitcoin mined in our operations or purchased in the open market, rather than selling bitcoin to generate revenue. In the second half of 2024, we raised approximately $2.2 billion, primarily through the issuance of the 2024 Convertible Notes, to acquire bitcoin as part of our HODL strategy. As a result, our financial condition is highly dependent on the market price of bitcoin, which historically has been volatile and subject to fluctuations due to regulatory developments, macroeconomic conditions,

15

technological advancements, security incidents, market speculation and adoption trends. If the price of bitcoin declines significantly or remains low for an extended period, the value of our holdings could decrease materially, affecting our balance sheet and liquidity. Since we do not generate significant revenue from other business activities, a prolonged downturn in bitcoin’s price could make it difficult to cover operational expenses, service debt or fund strategic initiatives. Additionally, if we need to sell bitcoin to meet financial obligations, we could face liquidity constraints, unfavorable market conditions or regulatory restrictions that limit our ability to do so. Any of these factors could adversely affect our financial stability and business prospects. While we believe our HODL strategy will create long-term value, there is no guarantee that it will generate the returns we expect or that we will be able to meet our obligations under outstanding convertible notes without negatively impacting our financial condition.

Significant disruptions in the cryptocurrency markets, like those in late 2022, could materially impair the value of our mining rigs, and prolonged low bitcoin prices could force us to idle mining rigs.

Major disruptions in the cryptocurrency market, such as those in late 2022, could significantly impact the value of our mining equipment. In the fourth quarter of 2022, bitcoin’s price fell from nearly $21,500 to a low of approximately $15,500. This decline, combined with negative market sentiment following the collapse of FTX Trading Ltd. in November 2022 and the bankruptcies and restructurings of multiple digital asset companies, caused a material decline in the fair value of our mining rigs and deposits for future mining rig purchases. As a result, we recorded a $332.9 million impairment charge for the quarter ended December 31, 2022. Similar market downturns in the future could force us to record further impairments on our current and future assets, which could negatively impact our financial condition.

Our ability to operate profitably depends heavily on bitcoin prices. If bitcoin’s price drops and remains low for an extended period, we may have to consider whether it is financially viable to continue operating certain mining rigs until prices recover. There is a theoretical minimum bitcoin price below which bitcoin mining becomes uneconomical, particularly when operating costs exceed mining revenue. However, determining this threshold is complex due to the constantly changing variables involved. We operate multiple mining sites with different hosting and electricity costs, each governed by separate contract structures. If market conditions make mining unprofitable across multiple sites, we may need to shut down or scale back operations, which could reduce our revenues and negatively impact our financial performance.

The adoption and long-term viability of digital asset networks is uncertain, and a decline in their growth or acceptance could negatively impact our business and the value of our stock.

Bitcoin and other digital assets are part of a new and rapidly evolving industry. The long-term growth and viability of digital assets depend on multiple factors, including:

•continued global adoption and usage of bitcoin and other digital assets;

•government regulations that impact digital asset transactions and network operations;

•the development and maintenance of Bitcoin’s open-source software protocol;

•shifting consumer demographics, preferences and payment habits;

•the availability and popularity of alternative payment methods, including improved fiat currency solutions;

•economic conditions and the regulatory environment for digital assets; and

•regulatory scrutiny and associated compliance costs.

If bitcoin adoption stagnates or declines, demand for bitcoin could weaken, which could negatively affect our business. A prolonged lack of growth in bitcoin adoption could reduce market confidence, leading to lower trading volumes and diminished liquidity. Additionally, bitcoin’s price volatility undermines its role as a medium of exchange, as retailers are less likely to accept it as a form of payment. Marketplace acceptance of bitcoin as a medium of exchange and payment method may remain low. The relative lack of acceptance of bitcoin in the retail and commercial marketplace, or a reduction of such use, limits the ability of end users to use bitcoin to pay for goods and services.

Further, as block rewards decrease, higher transaction fees may be required to incentivize miners, potentially reducing bitcoin adoption and value. In order to incentivize miners to continue to contribute processing power to any digital asset network, such network may either formally or informally transition from a set reward to transaction fees earned upon solving for a block. This transition could be accomplished either by miners independently electing to

16

record in the blocks they solve only those transactions that include payment of a transaction fee or by the digital asset network adopting software upgrades that require the payment of a minimum transaction fee for all transactions. If transaction fees paid for digital asset transactions become too high, the marketplace may be reluctant to accept digital assets as a means of payment and existing users may be motivated to switch from one digital asset to another digital asset or back to fiat currency. A decline in bitcoin transactions and adoption could reduce demand, negatively impacting bitcoin’s price and affecting the value of our bitcoin holdings.

We face risks related to technological obsolescence, vulnerability of the global supply chain for cryptocurrency hardware, potential trade restrictions and difficulty in obtaining new hardware, which may have a material adverse effect on our business.

Bitcoin mining hardware experiences wear and tear over time, requiring periodic repairs or replacement to maintain efficiency. Additionally, as mining technology evolves, we must invest in newer, more efficient mining equipment to remain competitive, which requires significant capital expenditures.

Further, we have faced complications related to the import of mining equipment in the past and may face such complications in the future. The global supply of miners is unpredictable and presently heavily dependent on manufacturers based in China. Geopolitical matters, including the relationship between the United States and other countries and trade restrictions and tariffs (or the threat of trade restrictions or tariffs), may impact our ability to import miners or other equipment necessary for our operations. Restrictions or bans on mining equipment from China, whether due to trade restrictions, national security concerns or geopolitical tensions, could disrupt our supply chain, increase equipment costs and delay our growth plans.

In addition, officials of the U.S. Customs and Border Protection agency (“CBP”) have broad discretion regarding products imported into the United States, and the CBP has on occasion detained or seized imported miners and other equipment necessary to the operation of our miners, which has resulted in significant costs to us. If our imported mining equipment is detained or seized in the future, we may not be able to obtain adequate replacement parts for our existing miners and other equipment or obtain additional miners and other equipment from manufacturers on a timely basis or at all, which could have a material adverse effect on our results of operations and financial condition.

We may experience liquidity constraints and need additional capital, which may not be available to us on favorable terms, or at all.

Liquidity risk is the possibility that we will be unable to meet our financial obligations as they come due. To manage this risk, we use a planning and budgeting process to estimate the funds needed for ongoing operations and growth initiatives. In 2024, we settled our obligations using cash, cash equivalents and net proceeds from our offerings of the 2024 Convertible Notes and stock sales pursuant to our at-the-market offerings. Additionally, in October 2024, we secured a $200.0 million line of credit through master lending agreements with a consortium of lenders. This line of credit requires digital asset collateral, but since these agreements are uncommitted, we cannot guarantee access to funds on commercially reasonable terms or at all. Further, if bitcoin’s price drops significantly, we may face margin calls on our borrowings, requiring us to post additional collateral or risk liquidation of collateralized bitcoin.

We expect that we will need to raise additional capital to expand our operations, pursue our growth strategy and respond to competitive pressures or unanticipated working capital requirements. We may seek but fail to obtain additional debt or equity financing on favorable terms, if at all, which could impair our growth and adversely affect our existing operations. Raising capital through equity financing could dilute existing stockholders and reduce the value of their investment. Debt financing, on the other hand, could impose restrictive terms, prioritize creditors over stockholders or require us to maintain liquidity levels or financial ratios that may not align with our business needs or be in the best interest of our stockholders.

Our bitcoin lending arrangements expose us to risks of borrower default, operational failures and cybersecurity threats.

From time to time, we generate income through bitcoin lending, which carries significant risks. The volatility of bitcoin increases the likelihood that borrowers may default due to market downturns, liquidity crises, fraud or other financial distress. Because our bitcoin lending arrangements are unsecured, they rank below secured debt in a

17

borrower’s capital structure. If a borrower becomes insolvent, we may be unable to recover the loaned bitcoin, leading to substantial financial losses.

Additionally, digital asset lending platforms are vulnerable to operational and cybersecurity risks. Technical failures, software bugs or system outages could disrupt lending activities, delay transactions or result in inaccurate record-keeping. Cybersecurity threats, including hacking, phishing and other malicious attacks, pose further risks, potentially leading to the loss, theft or misappropriation of our loaned bitcoin. A successful cyberattack or security breach could materially and adversely impact our financial position, reputation and ability to conduct future lending activities.

The U.S. political and economic environment could materially impact our business operations and financial performance, and uncertainty surrounding the potential legal, regulatory and policy changes by the new U.S. presidential administration may directly affect us and the global economy.

Changes in U.S. political leadership and economic policies may create uncertainty that materially affects our business and financial performance. Shifts in legal, regulatory, and trade policies, particularly under a new presidential administration, could disrupt our operations and long-term strategy.

For example, if the U.S. government establishes a strategic bitcoin reserve, large-scale purchases could create price volatility or artificial price suppression, making our mining operations less profitable. Conversely, slow or no action in creating such a reserve could limit institutional adoption and negatively impact bitcoin’s value, which could also harm our financial condition. Additionally, increased government influence over the Bitcoin network could affect mining difficulty, transaction processing, and other technical aspects, further impacting our business.

We also face risks from trade policy changes, including tariffs and restrictions on imports of mining equipment. The current administration has imposed, and may continue to impose, tariffs on imports from key manufacturing regions, increasing costs and disrupting supply chains.

The scope and timing of potential policy changes remain uncertain, making it difficult to plan for or mitigate these risks. Any such changes could materially and adversely affect our business, financial condition, and results of operations.

We have engaged in, and may continue to engage in, strategic acquisitions and other transactions that could disrupt our business, dilute our stockholders, strain our financial resources and harm our operating results.

As part of our growth strategy, we have pursued strategic transactions, including acquiring companies, miners and data centers. In the future, we may seek additional opportunities to expand our mining operations, including purchasing miners, data centers and other facilities, potentially from companies in financial distress. Our ability to grow through acquisitions depends on several factors, including the availability of suitable opportunities at acceptable costs, our ability to compete effectively to attract those opportunities and access to financing.

Acquisitions may require us to issue common stock, thereby diluting existing stockholders, or take on liabilities from acquired businesses. They may also result in recording goodwill and intangible assets that require regular impairment testing, which could lead to periodic write-downs. Additionally, acquisitions often involve significant costs, including integration expenses, restructuring charges and potential litigation risks.

Even when successful, acquisitions and expansions may take considerable time to deliver anticipated benefits, if at all. Integrating new businesses, technologies, and personnel can be complex and may divert management’s attention from daily operations. We may also face liabilities related to a target company’s past operations. Entering new markets where we have little experience could pose additional challenges, particularly if competitors have stronger market positions. Furthermore, we may struggle to generate sufficient revenue to justify acquisition costs, and the integration process could disrupt relationships with employees, suppliers and other stakeholders.

Further, we may not be able to pursue our current acquisition strategy in the future. Beyond bitcoin mining and related acquisitions, we have explored, and may continue to explore, opportunities in adjacent or complementary businesses as market conditions allow. These ventures may carry similar risks, including operational and financial challenges, and there is no guarantee they will provide the expected benefits in a timely manner, if at all.

18

Geopolitical and economic crises could lead to increased uncertainty, large-scale selloffs of digital assets and a decline in bitcoin’s value, negatively impacting our business and stock price.

Bitcoin is an alternative to fiat currencies that are backed by central governments, but its value is highly dependent on supply and demand. It is unclear how global geopolitical and economic crises will affect the adoption and valuation of digital assets. However, such crises may lead to large-scale acquisitions or sales of digital assets, causing significant price volatility. A large-scale selloff of bitcoin could decrease its value, directly affecting our business and the price of our common stock. Additionally, broader macroeconomic instability, inflation and regulatory uncertainty could impact our ability to conduct business efficiently and profitably. A significant decline in bitcoin’s value due to economic or geopolitical factors could negatively affect our financial condition.

The lack of legal recourse and insurance for our digital assets increases the risk of total loss in the event of theft or destruction.

Our digital assets are not insured against theft, loss or destruction. If an event occurs where we lose our digital assets, whether due to cyberattacks, fraud or other malicious activities, we may not have any viable legal recourse or ability to recover the lost assets. Unlike funds held in insured banking institutions, our digital assets are not protected by the Federal Deposit Insurance Corporation or the Securities Investor Protection Corporation. If our digital assets are lost under circumstances that render another party liable, there is no guarantee that the responsible party will have the financial resources to compensate us. As a result, we and our stockholders could face significant financial losses.

The open-source structure of the Bitcoin network exposes us to risks related to software development, security vulnerabilities and potential disruptions.

Digital asset networks are open-source projects and, although there is an influential group of leaders in, for example, the Bitcoin network community known as the “Core Developers,” there is no official developer or group of developers that formally controls the Bitcoin network. As an open-source project, Bitcoin is not represented by an official organization or authority. The Bitcoin network protocol is not sold, and contributors generally are not compensated for maintaining and updating the Bitcoin network protocol. Without guaranteed financial incentives, there may be insufficient resources to address emerging issues, upgrade security or implement necessary improvements in a timely manner. If the Bitcoin network’s software is not properly maintained or developed, it could become vulnerable to security threats, operational inefficiencies and reduced trust, all of which could negatively impact bitcoin’s long-term viability and our business.

Bitcoin network forks, where the blockchain splits into two separate networks, could cause disruptions and negatively impact our business.

Since the Bitcoin network is an open-source project, any individual can download the Bitcoin network software and make any desired modifications, which are proposed to users and miners on the Bitcoin network through software downloads and upgrades and typically posted to the Bitcoin development forum on GitHub.com. A substantial majority of miners and Bitcoin users must consent to those software modifications by downloading the altered software or upgrade that implements the changes. Otherwise, the changes do not become a part of the Bitcoin network.

Since the Bitcoin network’s inception, changes to the network have been accepted by the vast majority of users and miners, ensuring that the network remains a coherent economic system. However, a developer or group of developers could propose a modification to the Bitcoin network that is not accepted by a vast majority of miners and users, but that is nonetheless accepted by a substantial population of participants in the Bitcoin network. In such a case, and if the modification is material or not compatible with the prior version of Bitcoin network software, a fork in the blockchain could develop and two separate Bitcoin networks could result with one running the pre-modification software program and the other running the modified version (i.e., a second “Bitcoin” network).

Historically, the Bitcoin community has worked to merge forked blockchains, but a prolonged or unresolved split could create confusion, disrupt the network and affect bitcoin’s stability. A fork could decrease confidence in bitcoin, negatively impacting its price and, in turn, our business and stock value.

19

Widespread delays in the recording of transactions could erode confidence in the Bitcoin network and negatively impact our business.

To the extent that any miners cease to record transactions in solved blocks, such transactions will not be recorded on the Bitcoin blockchain, until a block is solved by a miner who does not require the payment of transaction fees. Currently, there are no known incentives for miners to actively not record transactions in solved blocks. However, to the extent that any such incentives arise (e.g., a collective movement among miners or one or more mining pools forcing blockchain users to pay transaction fees as a substitute for or in addition to the award of new bitcoin upon the solving of a block), actions of miners solving a significant number of blocks could delay the recording and confirmation of transactions on the blockchain. Widespread delays could increase the risk of “double-spending” (i.e., spending the same digital assets in more than one transaction), reduce trust in the network, and negatively impact bitcoin’s adoption and price. This could, in turn, affect the value of our bitcoin holdings and our financial performance.

Our reliance on third-party mining pools for a portion of our mining revenue exposes us to operational and financial risks.

While we rely largely on our internal mining pool, we additionally rely on external open-access mining pools to receive certain mining rewards and fees from the Bitcoin network. External pools have the sole discretion to modify the terms of our agreement at any time, and, therefore, our future rights and relationship with such pools may change.

In general, mining pools allow miners to combine their computing and processing power, increasing their chances of solving a block and getting rewarded by the Bitcoin network. The rewards are distributed by the pool operator proportionally to our contribution to the pool’s overall mining power. Should any external pool’s operator systems suffer downtime due to cyber-attacks, software failures or operational issues, our ability to mine and receive revenue would be negatively impacted. Furthermore, while we receive daily reports from the external pools detailing the total processing power provided to the pool and the proportion of that total processing power we provided to determine the distribution of rewards to us, we are dependent on the accuracy of each such pool’s recordkeeping. We have minimal recourse against external pool operators if we determine the proportion of the reward paid out to us by the mining pool operator is incorrect, aside from leaving the pools. If we cannot consistently obtain accurate proportionate rewards, our business and financial performance could suffer.

A 51% attack on the Bitcoin network could undermine security and market confidence.

The security of the Bitcoin network relies on its decentralized nature, which makes it difficult for any single entity to control a majority of the network’s mining power. However, if a malicious actor or coordinated group were to gain control of more than 50% of the total hashrate, a scenario known as a “51% attack,” they could theoretically manipulate the network by:

•reversing previously confirmed transactions, enabling double-spending of bitcoin;

•preventing new transactions from being confirmed, effectively halting the network; and

•excluding or modifying transactions, undermining the trustworthiness of the blockchain.

A 51% attack could occur through several mechanisms, including large-scale mining operations, through which a single entity invests in expansive mining facilities with enough computing power to control the majority of the network; mining pool dominance, in which mining pool becomes so large that it collectively controls more than 50% of the network’s hashrate; or botnet-based attacks, in which botnets (volunteers or hacked collections of computers controlled by networked software coordinating the actions of the computers) are used to hijack computing resources and direct them toward mining, effectively amassing enough power to launch an attack.

If a 51% attack were successfully executed, it could lead to a loss of confidence in bitcoin’s security and reliability, causing its price to drop significantly. Such an event could also prompt regulatory restrictions on cryptocurrency mining and trading, further exacerbating the negative impact on our business.

Even if a 51% attack does not occur, the mere perception that such an attack is possible could damage bitcoin’s credibility and discourage institutional adoption. Given our dependence on bitcoin mining, any loss of trust in the

20

security of the Bitcoin network could materially and adversely affect our business, financial condition and results of operations.

The scheduled reduction of bitcoin mining rewards due to halving events may decrease our revenue and could force us to cease mining operations.

Bitcoin undergoes a process known as “halving,” which reduces the reward miners receive for successfully mining a block. This process is designed to control the total supply of bitcoin and occurs approximately every four years. The most recent halving in April 2024 reduced mining rewards from 6.25 to 3.125 bitcoin per block, with the next halving expected in April 2028. Halvings are expected to continue until the total bitcoin supply reaches 21,000,000 bitcoin, projected around the year 2140.

Bitcoin prices have fluctuated around past halving events, and there is no guarantee that future halvings will result in price increases sufficient to offset reduced mining rewards. If bitcoin prices do not increase proportionately, our mining revenue may decline, potentially making continued operations financially unsustainable. If we reduce or cease mining, our business would be materially harmed, and investors could suffer a complete loss of their investment.

Further, reduced bitcoin mining incentives due to halving events may weaken network security and adversely affect our operations. Lower mining rewards could lead to a decrease in the hashrate securing the Bitcoin network if miners shut down operations due to reduced profitability. A lower hashrate could slow transaction confirmations and make the network more susceptible to malicious actors gaining control of 50% or more of the total processing power, increasing the risk of fraudulent transactions. Any weakening of Bitcoin network security could negatively impact our operations and harm investor confidence in our securities.

High operating costs and the need for professionalized mining operations may lead to downward pressure on bitcoin prices.

Over the past three years, digital asset mining operations have evolved from individual users mining with computer processors, graphics processing units and first-generation mining rigs. New processing power brought onto the digital asset networks is predominantly added by professionalized mining operations, which may use proprietary hardware or sophisticated machines. Professionalized mining operations require:

•significant capital investment tin specialized hardware;

•leasing operating space (often in data centers or warehousing facilities);

•substantial electricity consumption; and

•employing technicians to operate the mining sites.

Unlike past individual miners who may have held mined bitcoin for extended periods, professionalized mining operations typically sell newly mined bitcoin immediately to cover ongoing expenses. If mining profitability declines, professional miners may sell even more bitcoin into the market, increasing supply and potentially driving down bitcoin prices. If this price decline is significant, it could further reduce mining profitability, leading to additional sell-offs and a negative feedback loop that could harm our business and adversely affect an investment in our securities.

Our increasing reliance on immersion-cooling technology exposes us to operational and regulatory risks.

We are expanding our use of immersion-cooling technology for bitcoin mining, particularly at our Granbury, Texas facility. Immersion-cooling is an emerging, relatively untested technology at scale within the bitcoin mining industry, and we may face challenges in achieving the expected cooling performance. If we fail to optimize our immersion-cooling systems, our mining efficiency and profitability may suffer.

In addition, regulation of certain perfluoroalkyl and polyfluoroalkyl substances, collectively known as “PFAS,” may affect our operations. Governments in the United States and internationally have increased their focus on and regulation of PFAS which are present in some coolants used in our immersion-cooling systems. Developments in global chemical regulatory trends (including relating to PFAS) could lead to additional compliance costs, potential litigation, or operational disruptions, all of which could adversely affect our operations and financial condition.

21

Loss of access to our private keys or data could result in a permanent loss of our digital assets.

Digital assets are controllable only by the possessor of both the unique public key and private key relating to the local or online digital wallet which hold the digital assets. We are required by the operators of digital asset networks to publish the public key relating to a digital wallet in use once we first verify a spending transaction from that digital wallet and broadcast such information into the respective network. We safeguard the private keys relating to our digital assets by relying on four custody providers, including New York Digital Investment Group LLC (“NYDIG”). To the extent a private key is lost, destroyed or otherwise compromised and no backup of the private key is accessible, we would be unable to access the digital assets and the private key would not be capable of being restored by the respective digital asset network. Any loss of private keys relating to digital wallets used to store our digital assets could adversely affect an investment in our securities.

Cybersecurity threats, including hacking and malware, could result in loss of digital assets, reputational damage, and business disruptions.

The digital asset industry is a frequent target for cyberattacks, including:

•unauthorized access to systems and data;

•intentional corruption, destruction, or loss of digital assets; and

•social engineering attacks targeting employees

A successful cybersecurity breach could result in the theft or loss of our bitcoin holdings, disruptions to our mining operations and significant reputational harm. As our digital asset holdings grow, we may become a more attractive target for cybercriminals, further increasing our risk exposure.

We rely on third-party custody providers’ solutions to safeguard digital assets from theft, loss, destruction or other issues relating to cyberattacks. Notwithstanding the safeguards implemented to protect our assets, the third-party security systems may not be impenetrable or free from defect, and any loss due to a security breach, software defect or event outside of our control will be borne by us.

Our systems and operational infrastructure may be breached due to the actions of outside parties, error or malfeasance of an employee or otherwise, and, as a result, an unauthorized party may obtain access to our private keys, data or digital assets. Additionally, outside parties may attempt to fraudulently induce our employees to disclose sensitive information in order to gain access to our systems or infrastructure.

Despite our efforts, we may be unable to anticipate security breaches, including cyberattacks, or implement adequate preventative measures since the hacking techniques used often are not recognized until launched against a target. If an actual or perceived breach of our security systems occurs, the market perception of the effectiveness of our controls could be harmed, which could adversely affect an investment in our securities.